Number of retirees saying they have enough money for everything they want falls 13 points from 2015

June 16, 2025 – The Canada Pension Plan Investment Board (CPPIB) ended the fiscal year with net assets of more than $714 billion. Despite the nest egg however, the nation’s largest pension fund has faced criticism in recent months, for its investment strategy that some say doesn’t focus enough on domestic projects. Indeed, as Prime Minister Mark Carney focuses his attention on “nation-building” projects, some have suggested that CPPIB should play a bigger role in funding those endeavours.

New data from the non-profit Angus Reid Institute finds Canadians cool to this concept if it comes with lower returns. Asked if they feel the fund should invest wherever it earns the greatest returns or invest more in Canada, seven-in-10 (72%) say fiduciary obligations should remain paramount. These views are relatively consistent across age and income levels, as well as retirement status. Current just 12 per cent of CPPIB assets are invested domestically.

These data come as the challenges faced by retirees and expected by those preparing for that phase of their life appear to have grown over the past decade. The proportion of retirees saying they have enough money for everything they want has dropped by one-third, from 38 to 25 per cent since 2015, with a corresponding 16-point increase in the number saying they’re “comfortable” but don’t have money for luxuries. One-in-seven (15%) say making ends meet is a struggle.

Among those who have yet to retire, the proportion saying they expect a challenge in getting by has risen by one-third, from 28 to 38 per cent over the same period.

Why is the CPPIB so important? Consider that among the unretired, one-quarter say they will be “heavily reliant” on these benefits, while another half say it will be important to their livelihood.

INDEX

Part One: Where should the CPPIB invest?

Part Two: Retirement and expectation

- Retirees

- Expectations from the non-retired

- Funding retirement

Part Three: Economic outlook

- Update on more current economic trends

Part One: Where should the CPPIB invest?

As Canada looks to build its domestic economy and reverse the trend of stagnating growth, some have proposed that the nation’s largest pension fund, the CPPIB, should have more of a focus on investing in Canada. As of March 2025, 12 per cent of the fund’s $714.4 billion assets were invested in Canada. The CPPIB was established via the Canada Pension Plan Investment Board Act in 1997 after it was determined that employee contributions to CPP alone would not be a sustainable path to funding Canadians’ withdrawals in retirement. The current CPP mandate is “to maximize long-term investment returns without undue risk” and is country agnostic.

In 2023, former Finance Minister Chrystia Freeland proposed in the fall economic statement that she was considering encouraging Canadian pension funds to invest more at home.

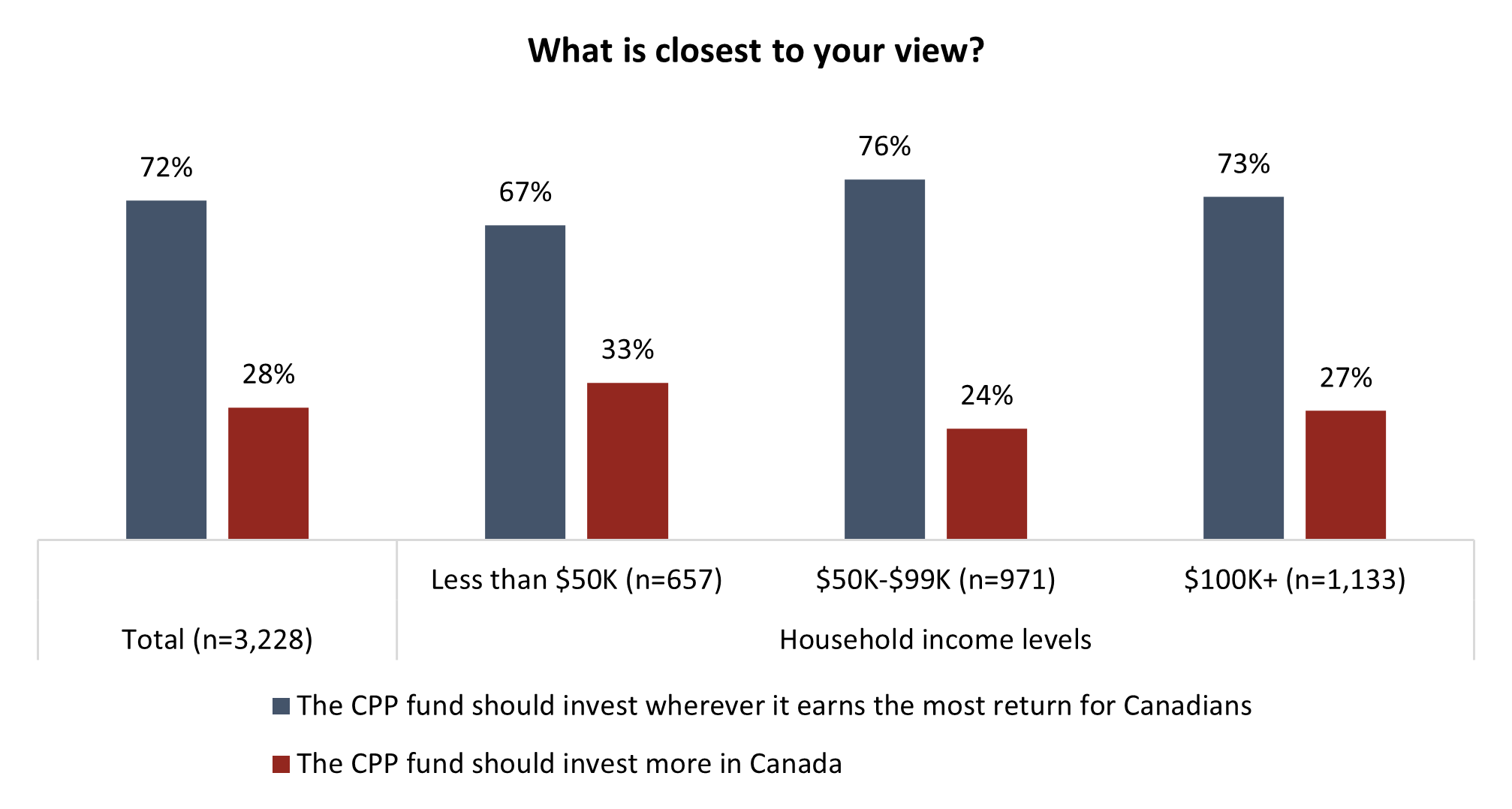

Canadians, by an almost three-to-one margin, prefer the current arrangement. Seven-in-10 (72%) believe the CPP fund should invest “wherever it earns the most return for Canadians”, while more than one-quarter (28%) believe the fund should have more of a Canadian focus.

The latter view is more likely to be held by Canadians in lower income households, but still two-thirds living in households earning less than $50,000 annually believe maximizing returns should be the focus:

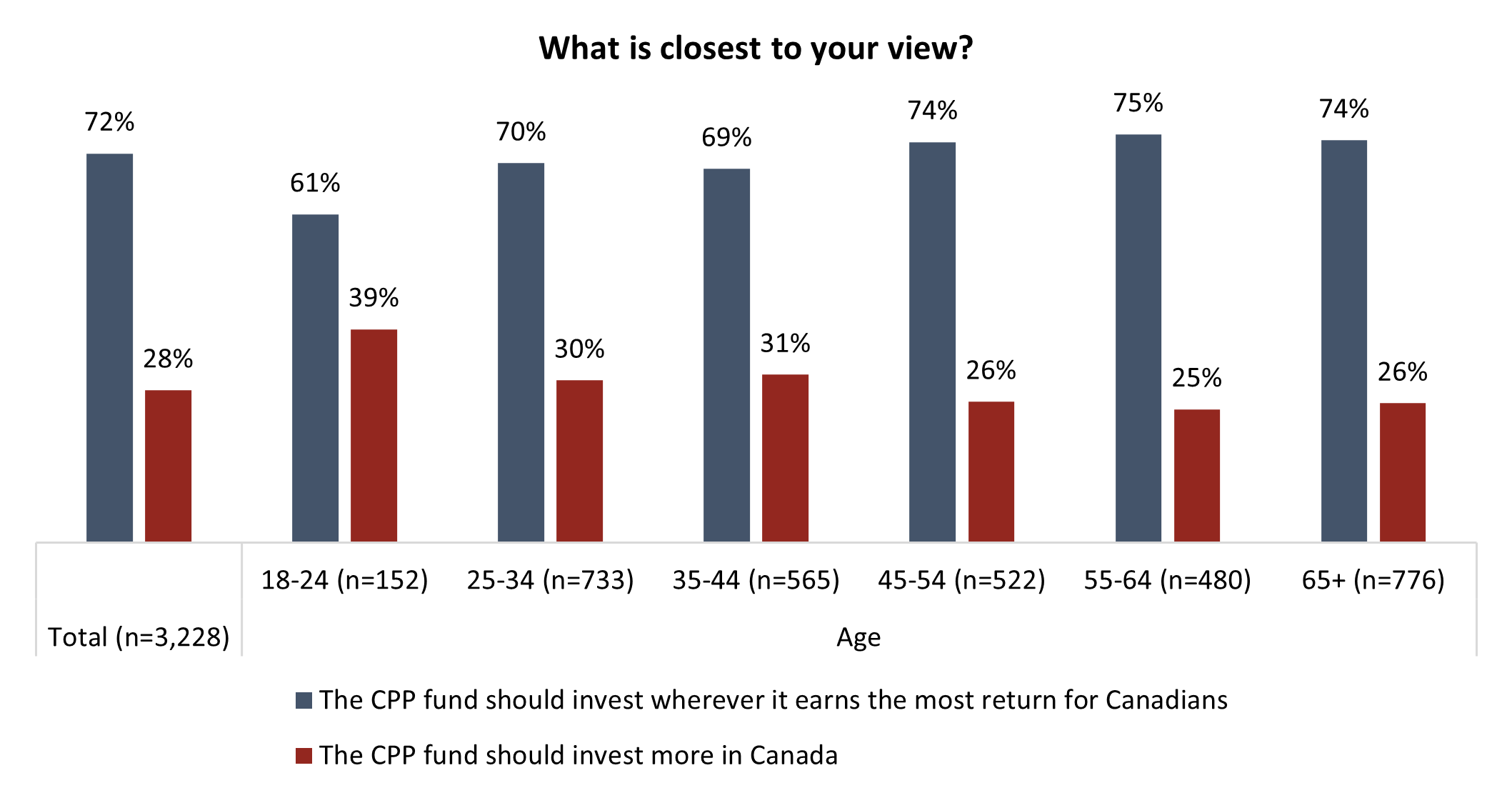

A majority of all age groups believe the CPP fund should maximize returns for Canadians, regardless of where those returns might be. But the youngest Canadian adults, and it should be noted the furthest away from retirement, are more likely to say they believe the CPP should invest more in Canada:

Part Two: Retirement and expectation

Retirees

CPP’s investments and disbursements are of course a hot button issue for the country’s retirees. Nearly one-in-five Canadians are 65 years of age or older, with many retired or semi-retired. And it comes during a time where the rising cost of living continues to be the top issue the country faces according to Canadians, despite the abatement of a period of high inflation not seen since the 1980s.

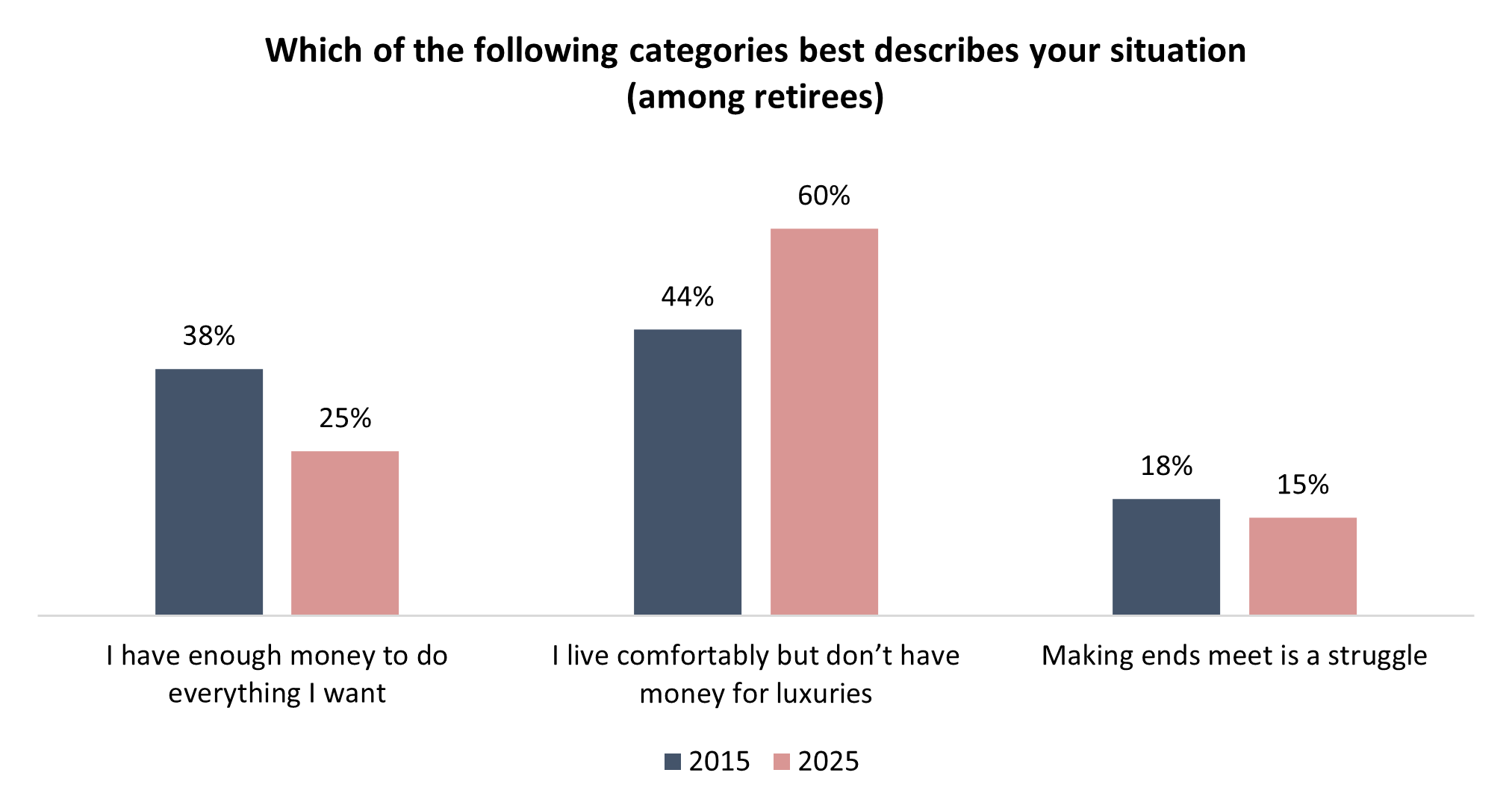

The majority (60%) of Canada’s retirees say they “live comfortably but don’t have money for luxuries”. One-in-six (15%) say making ends meet is a struggle, while a fortunate one-quarter (25%) say money isn’t an issue for them in their retirement.

The effect of the high cost of living is evident when you compare these figures to those taken 10 years ago by the Angus Reid Institute. In 2015, two-in-five (38%) retirees said they had enough in retirement to do what they want, while a slightly larger group (44%) said they forwent luxuries.

The proportion of Canadian retirees who say they are financially struggling in retirement has decreased slightly from 2015. While Prime Minister Justin Trudeau left office this year as a divisive figure, one of the things Canadians pointed to as a success for his nine-year term as PM was expanding the social safety net, including the dental care program, which benefitted many seniors.

Expectations from the non-retired

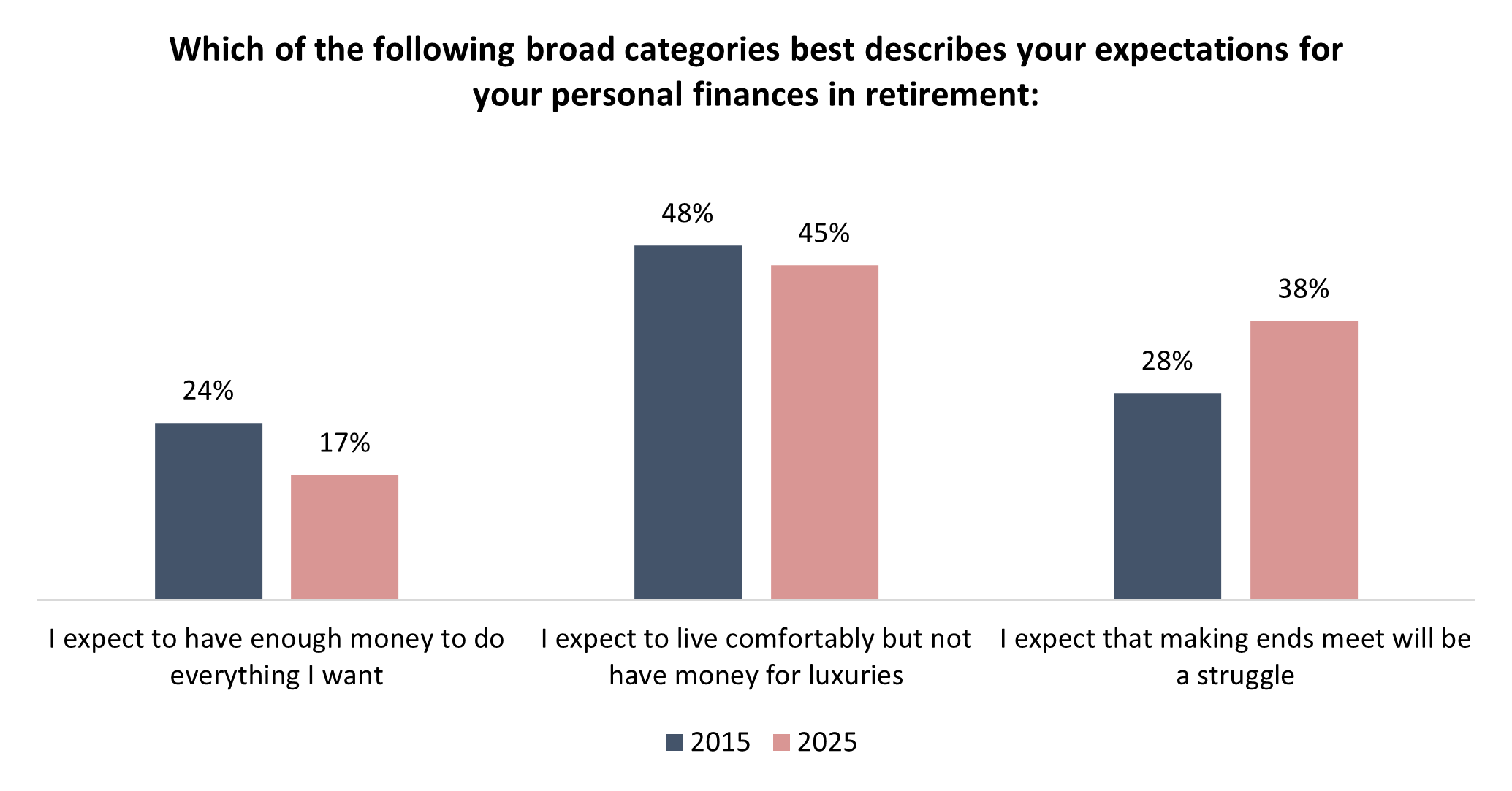

The realities for Canada’s retirees are rosier than the expectations from those still working. Two-in-five (38%) Canadians who have yet to retire say they expect they will struggle financially when they step away from the work force. Fewer than half (45%) say they expect to live comfortably, while one-in-six (17%) believe money won’t be an issue for them in their golden years.

Canadians’ pessimism about their future retired life has increased by 10 percentage points in the past decade. In 2015, three-in-ten (28%) expected that covering their costs would be a struggle once they retired. That proportional shift comes almost entirely from a drop of seven points among the group who expected money not to be an issue after they finished working:

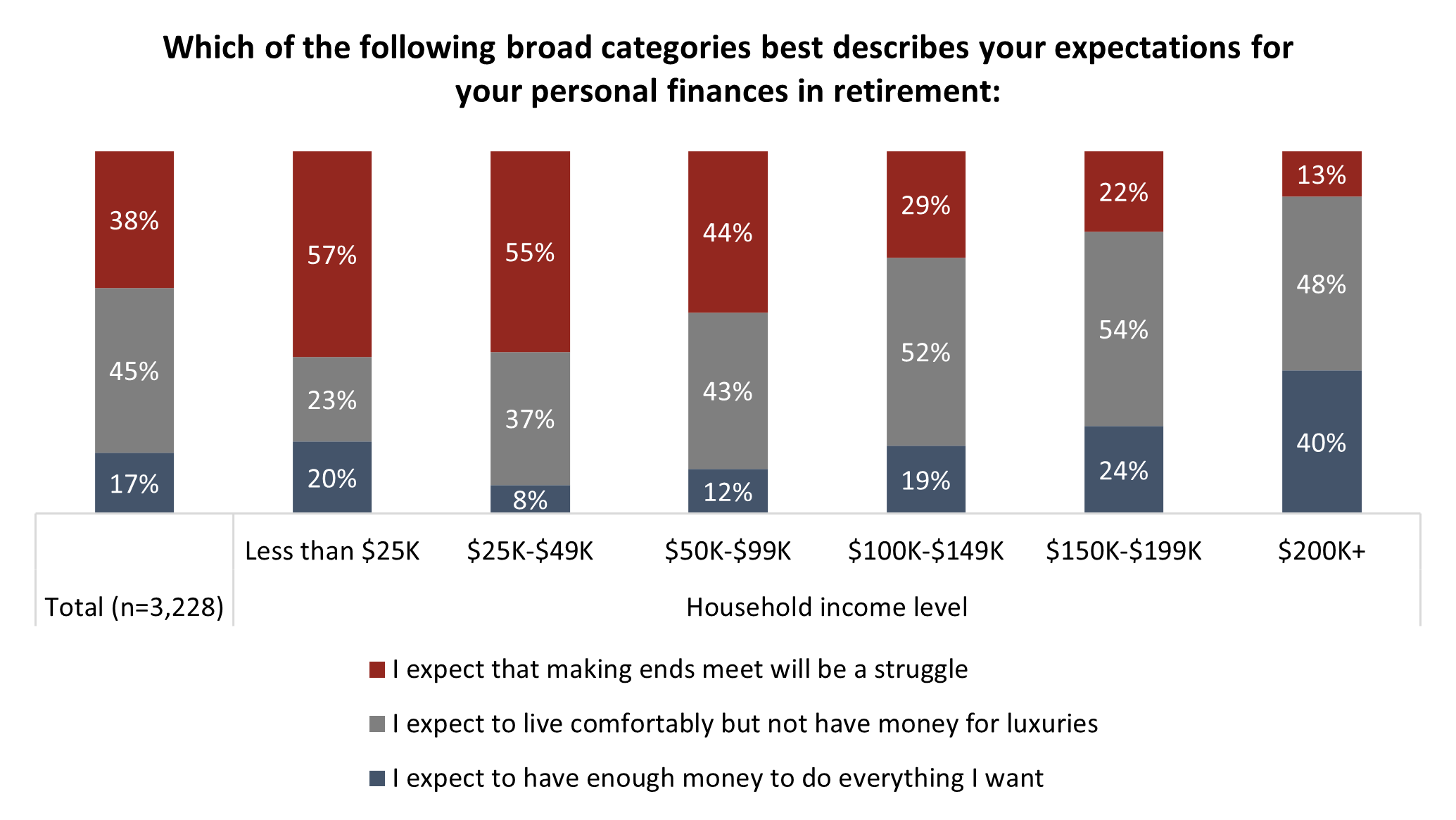

Household income is a significant determining factor for how pessimistic or optimistic Canadians are about their financial life in retirement. A majority of those in the lowest earning households in the country believe they will struggle financially when they are retired. Two-in-five in the highest income bracket believe they’ll have enough money to do what they want, but even more (48%) believe they won’t have money for luxuries in retirement:

Household income is a significant determining factor for how pessimistic or optimistic Canadians are about their financial life in retirement. A majority of those in the lowest earning households in the country believe they will struggle financially when they are retired. Two-in-five in the highest income bracket believe they’ll have enough money to do what they want, but even more (48%) believe they won’t have money for luxuries in retirement:

Funding retirement

Funding retirement

As the conversation continues over the CPPIB’s mandate, three-quarters of Canadians say they expect the CPP will play an important role for them financially when they retire. Just one-in-five say they have other savings that will primarily fund their retirement.

The ratio of Canadians who expect to rely on CPP versus those who do not is more or less similar to those seen a decade ago:

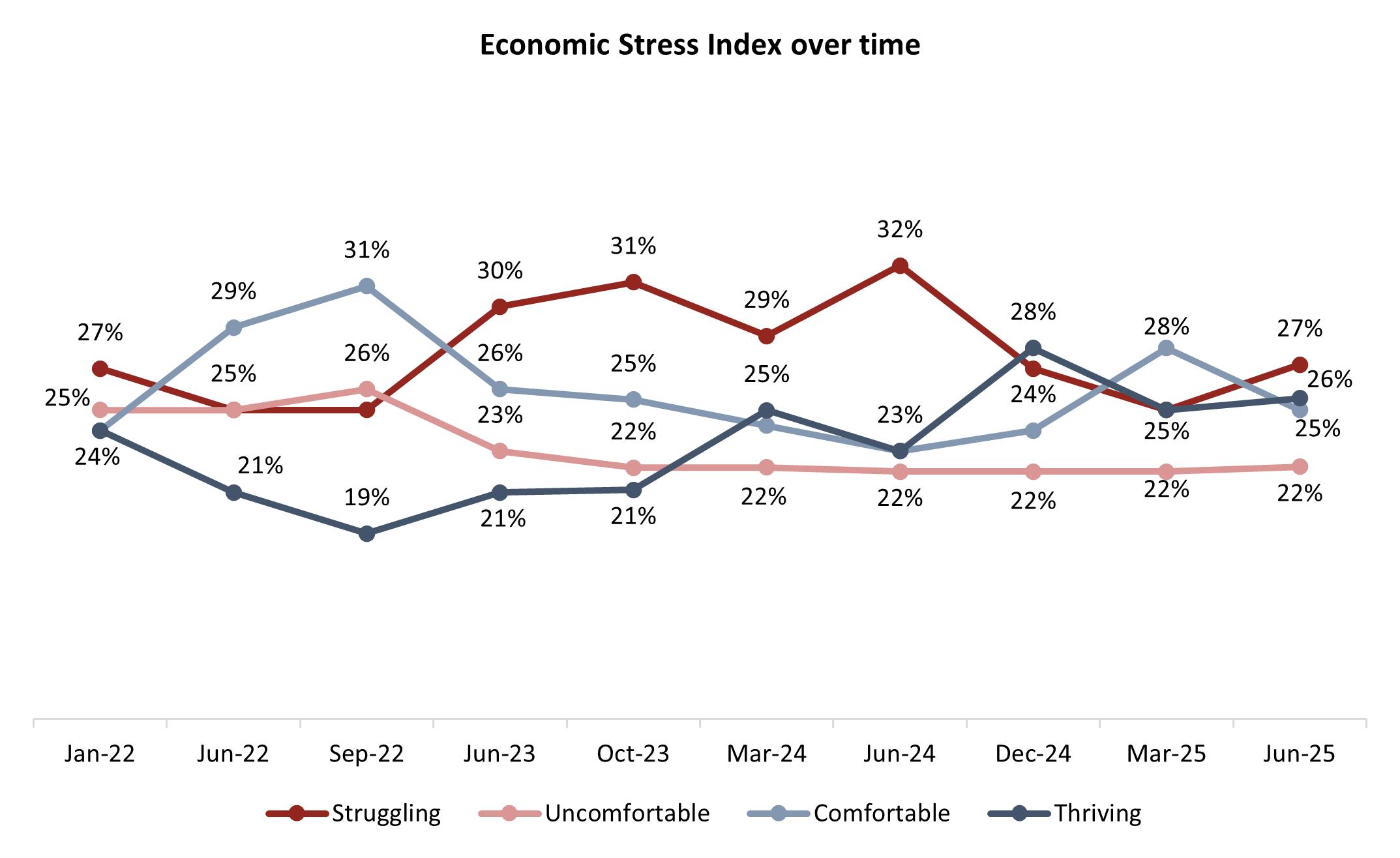

Since 2022, ARI has been measuring the Economic Stress Index, which assesses the financial pressure on Canadians through various questions about their personal finances and expectations.

Since 2022, ARI has been measuring the Economic Stress Index, which assesses the financial pressure on Canadians through various questions about their personal finances and expectations.

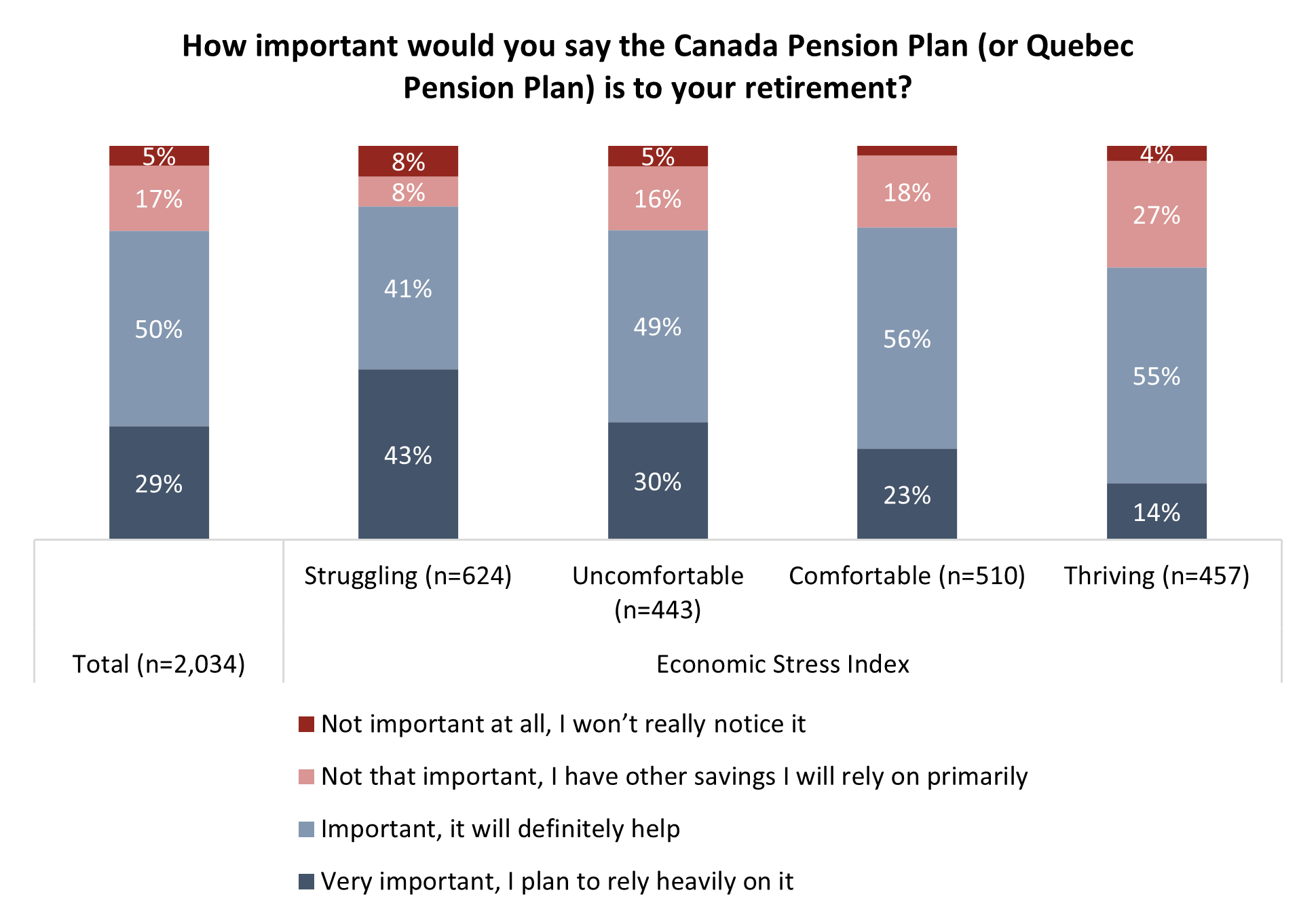

Canadians who are deemed Struggling by the Index are much more likely to say they will be relying heavily on CPP when they retire:

Retirement savings has been one of the casualties of the high cost of living Canadians have experienced recently. In 2023, the number of Canadians who said they were deferring contributing to a TFSA or RRSP had risen to 35 per cent from 22 per cent the year before.

Retirement savings has been one of the casualties of the high cost of living Canadians have experienced recently. In 2023, the number of Canadians who said they were deferring contributing to a TFSA or RRSP had risen to 35 per cent from 22 per cent the year before.

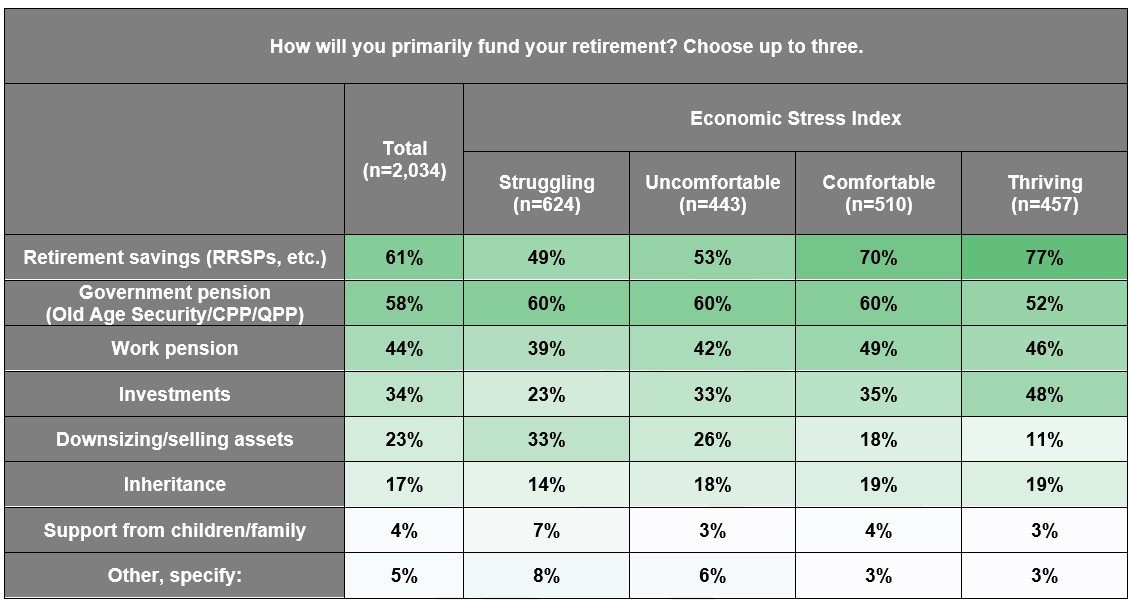

Canadians who are Thriving are much more likely to say their own retirement savings or investments will help fund their retirement than those who are Struggling. The latter group are much more likely to report they expect to be reliant on government pension programs:

Part Three: Economic outlook

Update on more current economic trends

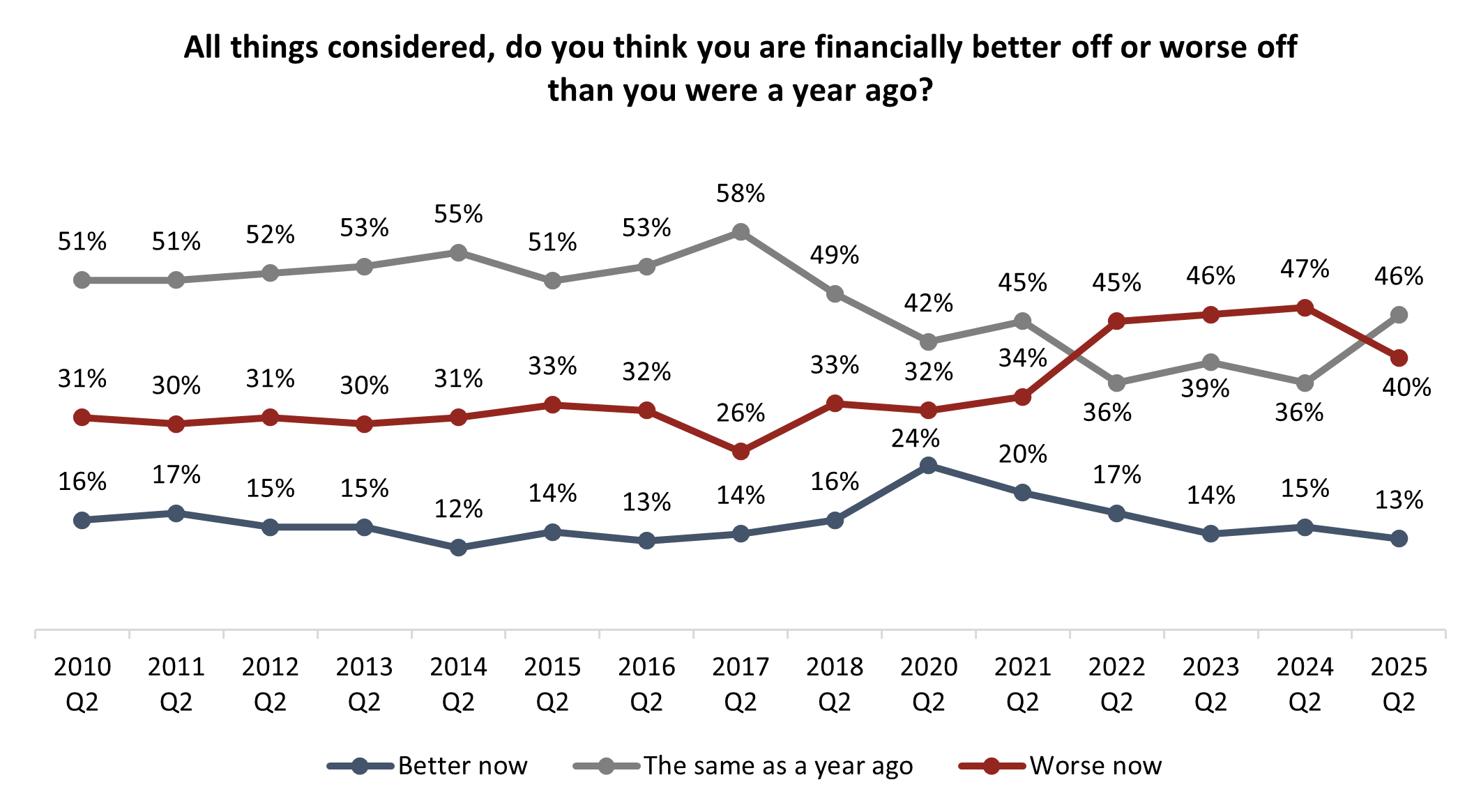

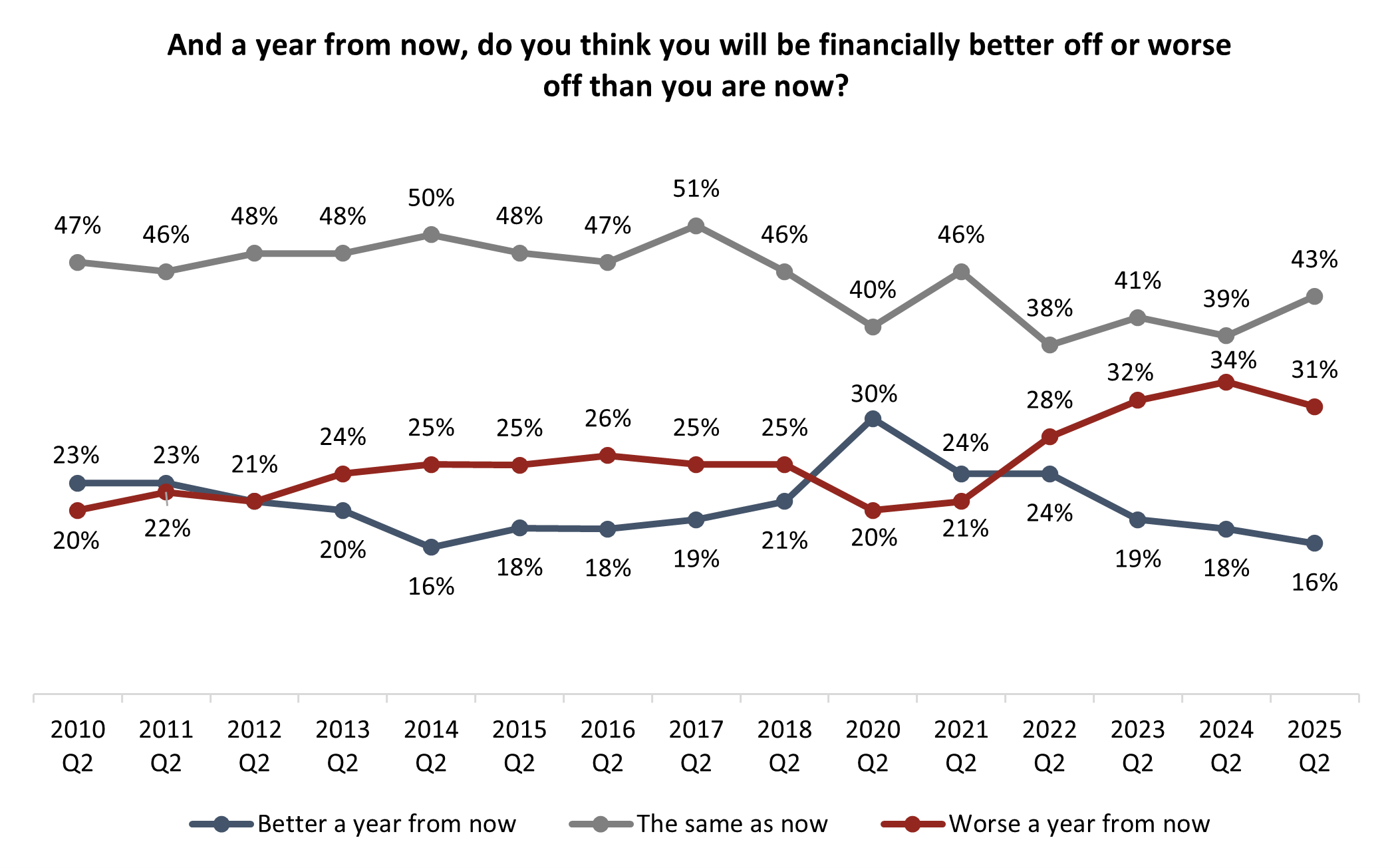

The new parliamentary session is one with a significant focus on the economy, growth, and increasing the ability of Canadians to trade and work across provinces. While the returns are early, the proportion of Canadians saying they are worse off now than they were at this time last year has fall seven points compared to 2024 data. There has been a 10-point increase in the number saying they’re about the same, and a two-point drop in the number saying they’re better off.

As for their level of optimism for the coming year, Canadians are still twice as likely to say that they expect to be worse off rather than better in June 2026. This net pessimism has persisted since 2022, while the largest number continue to expect no change:

Economic stress levels are relatively stable this quarter though we observe a slight increase in the proportion of Canadians “Struggling” on the ARI Economic Stress Index, at the cost a three-point decrease among the “Comfortable”.

Economic stress levels are relatively stable this quarter though we observe a slight increase in the proportion of Canadians “Struggling” on the ARI Economic Stress Index, at the cost a three-point decrease among the “Comfortable”.

METHODOLOGY:

The Angus Reid Institute conducted an online survey from June 2 – 5, 2025, among a randomized sample of 3,228 Canadian adults who are members of Angus Reid Forum. The sample was weighted to be representative of adults nationwide according to region, gender, age, household income, and education, based on the Canadian census. For comparison purposes only, a probability sample of this size would carry a margin of error of +/- 1.5 percentage points, 19 times out of 20. Discrepancies in or between totals are due to rounding. The survey was self-commissioned and paid for by ARI.

For detailed results by age, gender, region, education, and other demographics, click here.

For PDF of full release, click here.

For questionnaire, click here.

MEDIA CONTACTS:

Shachi Kurl, President: 604.908.1693 shachi.kurl@angusreid.org @shachikurl

Dave Korzinski, Research Director: 250.899.0821 dave.korzinski@angusreid.org

Jon Roe, Research Associate: 825.437.1147 jon.roe@angusreid.org