Most Canadians report retiring earlier or later because of circumstances beyond their control.

July 1, 2015 – Who is retiring? When in their lives are they doing it? How are they funding it? Are they satisfied with the experience? A comprehensive new Angus Reid Institute poll provides insights into these questions, and many others. Overall, the survey findings show that the Canadian retirement experience is vastly different for different groups of people, but largely fulfilling for most — notwithstanding quite widespread financial anxiety.

Key Findings:

- Less than half (46%) of retirees say

they retired when and as planned. The rest retired earlier (48%) or later (6%) because of circumstances outside their control.

they retired when and as planned. The rest retired earlier (48%) or later (6%) because of circumstances outside their control.

- Retired Canadians are considerably more reliant on government and work pensions to finance their retirement than still-working Canadians expect to be when they retire. And, while a fairly concerning one-half (48%) of the already retired are worried about outliving their money, this anxiety is shared by three-quarters (74%) of Canadians who are not yet retired.

- There is a fairly stark divide in the post-work experiences of public sector and private sector employees. Private sector retirees are nearly twice as likely to report they are “struggling” (22%) as those retired from the public sector (12%), who are, in turn, almost twice as likely to rely on a work pension (75%) as their private sector counterparts (39%).

- Retired Canadians express significant satisfaction with a number of key aspects of retirement. Indeed, four-in-ten say they have no regrets with life after work thus far. A large majority (more than nine-in-ten) enjoy having the time to relax and do what they want, which are areas of equally high expectations among the still-working crowd as well.

- Some retirees (roughly one-in-three) do wish they had closer community connections and better volunteer opportunities, as well as more time with family — though most are happy with these areas as well. Four-in-ten retirees admit to sometimes missing work, a concern shared by fully six-in-ten Canadians who are still working.

A special segmentation analysis places Canadian retirees into four broad groups, each displaying a distinct orientation towards retirement and each comprising roughly one-quarter of the retired Canadian population. The four groups are broadly summarized by their names: The “Lovin’ It” crowd, the Comfortable, the Strugglers and the Unhealthy.

PART 1: Anatomy and Financial Realities of Retirement

There are 6.4 million retired or semi-retired people in Canada, according to the Canadian Association of Retired People. They make up nearly a fifth of the overall population.

This special Angus Reid Institute study examined a number of key elements of what might be called the “anatomy of retirement” in Canada – with the main focus being on the circumstances precipitating retirement and Canadians’ financial security once out of the workforce. On both of these counts, the results paint a less-than-comforting picture of “the golden years.”

Early exits for many

First off, not even half (46%) of the retired Canadians surveyed controlled the circumstances surrounding their retirement – instead, as many (48%) said they “retired earlier due at least partly to circumstances outside my control”. Only a handful (6%) retired later than planned.

This syncs with the fairly young retirement ages reported in the survey. Overall, our retired sample splits into three groups: 36 per cent retired at age 55 or younger; 28 per cent retired in their late 50’s (between 56 and 60); and 36 per cent retired at 61 or older.

As would be expected, those who retired earlier than planned were younger still (44% of this group retired at 55 or younger) while the plurality (40%) of those who retired “when and as planned” worked until aged 61 or older.

Nationally, the average retirement age in 2014 was 63, though some specific economic sectors have averages that are higher or lower. According to Statistics Canada, the average retirement age has been rising slowly, but steadily, since 2010, when it was 62.1.

Retirees’ financial security

Financial security in retirement is part of the Canadian dream, but can hardly be taken for granted.

Nearly half (48%) of the retired Canadians surveyed agreed with the statement: “I’m worried about my money lasting my lifetime”; roughly one-in-five (19%) strongly agreed. This anxiety is shared by substantial numbers of retired Canadians from all walks of life – including more than half (54%) of retired women and retirees with less formal education (52%).

As bracing as this level of financial anxiety among retirees is, it is perhaps more remarkable that it is shared by roughly three-quarters (74%) of those not yet retired, more than a third of whom (36%) agree strongly with the statement.

Another survey item asked respondents to broadly describe how they are faring financially in retirement:

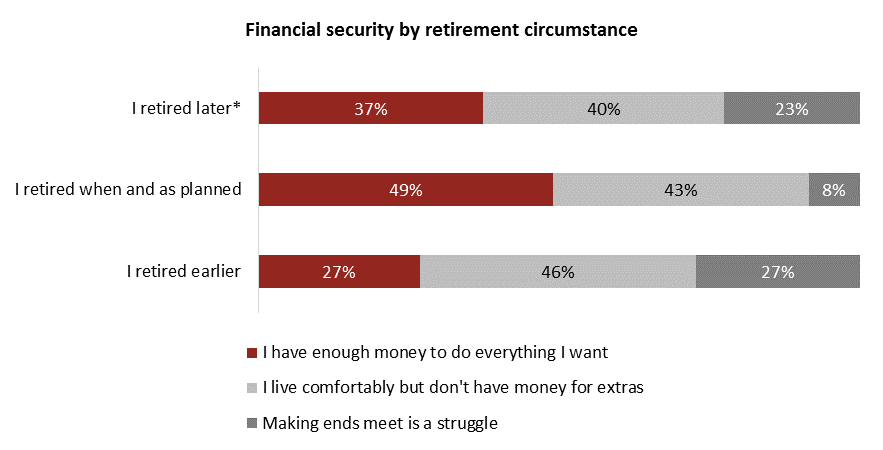

- Four-in-ten (38%) of the retired Canadians surveyed said “I have enough money to do everything I want”;

- A slightly larger group – 44 per cent – “live comfortably but don’t have money for extras”;

- And for the remaining one-in-five (18%) retired Canadians “making ends meet is a struggle”.

Of course, these two measures are highly correlated: fully nine-in-ten (90%) of those struggling to make ends meet are worried about outliving their money, whereas this concern is shared by fewer than one-in-five (17%) of those who say they have plenty of money. Importantly, most (58%) of those in the largest group (those who say they’re “comfortable”) share some anxiety about their money lasting their lifetime.

Freedom 55 – Really?

An early or younger exit from the workforce is not necessarily to be envied from a financial security perspective. The almost half (48%) of retirees who said they were forced by circumstance to retire earlier than planned are as likely to be struggling as they are to say they have enough money to do what they want – 27 per cent in each case, with the plurality (46%) opting for the middle option of “living comfortably.”

Compare this to those who retired when and as planned: 49 per cent say they have enough money to do whatever they want, four-in-ten (43%) are comfortable, and only one-in-ten (8%) is financially struggling.

*Small sample size

*Small sample size

How are Canadians financing retirement?

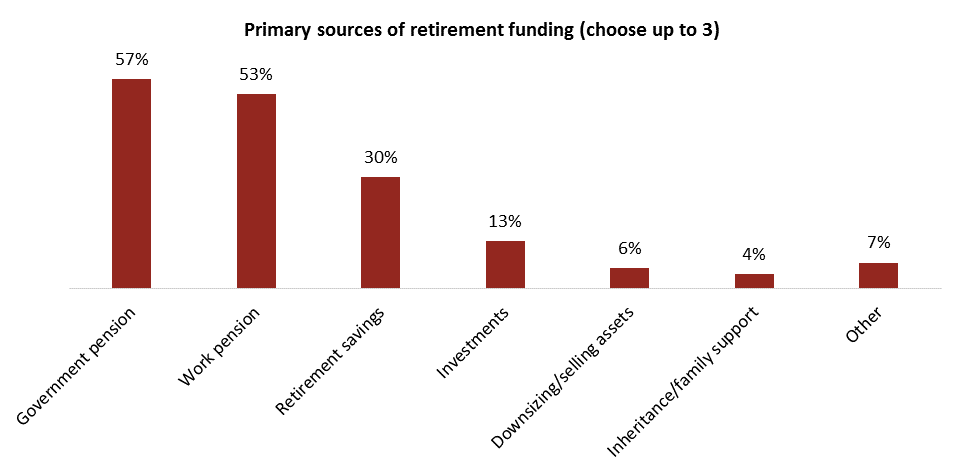

The Canadian retirees surveyed highlighted the following primary means of financing their retirement:

- Government pension – selected by 57 per cent as one of their three main sources of retirement income;

- A work pension – 53 per cent;

- Retirement savings (i.e.: RRSP’s, etc) – 30 per cent;

- Investments – 13 per cent;

- Downsizing/selling assets – 6 per cent;

- Other sources (including: inheritance, support from children, etc) – cited by a total of 11 per cent.

Of course, how one’s retirement is funded is strongly correlated with financial security:

- A government pension is a primary source of retirement income for two-thirds (67%) of those struggling to make ends meet versus less than half (43%) of those who describe themselves as well-off.

- And less than one-in-three (28%) of those struggling are able to rely on a work pension – whereas more than twice as many (61%) of the best-off group point to a work pension as a primary means of support.

- This affluent retired group is also considerably more likely to rely on retirement savings (40% do so) or investment income (25%).

- These two vehicles were cited much less often by the struggling group, who were more likely to say they have downsized (13% had done so) or used other means (such as support from children) to support themselves in retirement.

Public – Private sector divide

Running through all these results is a rather sharp divide between public sector and private sector retirees and, relatedly, between those who had been union members and those who had not. The marked difference in perspective lends considerable credence to arguments about a growing inequity between Canada’s public and private sector workers. Consider the following:

- Private sector retirees are considerably more likely to report leaving the workforce early due at least partly to circumstances outside their control (53% versus 41%).

- They are almost twice as likely to report that making ends meet is a struggle (22% versus 12%).

- Private sector retirees are also more likely to worry about outliving their money (53% versus 41%).

- And, of course, public sector retirees are much more likely to be relying on a work pension as a primary support in their retirement (75% versus 39%) whereas their private sector counterparts are more likely to be relying on other savings and supports. (Both groups, significantly, cite Canadian government pensions as a main source of retirement support – 57% each.)

A very similar pattern is noted by union membership history – reflecting the reality of public versus private sector unionization in Canada today.

| Did you control the circumstances of your retirement? | ||

|---|---|---|

| Public Sector | Private Sector | |

| I retired earlier due at least partly to circumstances outside my control | 41% | 53% |

| I retired when and as planned | 55% | 40% |

| I retired later due at least partly to circumstances outside my control | 4% | 8% |

| What best describes your situation? | ||

| Public Sector | Private Sector | |

| I have enough money to do everything I want | 44% | 34% |

| I live comfortably but don’t have money for extras | 44% | 44% |

| Making ends meet is a struggle | 12% | 22% |

| I’m worried about my money lasting my lifetime. | ||

| Public Sector | Private Sector | |

| Strongly agree/Agree | 41% | 53% |

| Strongly disagree/Disagree | 59% | 47% |

| What are your main sources of retirement income? | ||

| Public Sector | Private Sector | |

| Government pension (Old Age pension) | 57% | 57% |

| Work pension | 75% | 39% |

| Your retirement savings (RRSPs, etc) | 22% | 35% |

| Investments | 9% | 15% |

| Downsizing/selling assets | 5% | 6% |

| Inheritance | 1% | 4% |

| Support from children/family | 1% | 1% |

| Other, specify | 2% | 10% |

PART 2: Working Canadians’ Plans and Expectations

The expectations of Canadians who are not yet retired are somewhat at odds with some of the important retirement realities highlighted by the Angus Reid Institute survey of retirees.

- For example, retirement age. Most Canadians not yet retired (72%) expect to work into their 60’s, but almost half (45%) would prefer to retire by age 55 – the gap here perhaps reflecting the reality of financial insecurity being experienced by many who did retire younger, often not entirely by their own choosing. Somewhat ironically, given the public-private sector divide discussed earlier, public sector and union workers are decidedly keener about retiring earlier than they actually expect to, whereas their private sector and non-union counterparts are more likely to be fine with working into their 60’s.

- Interestingly, the non-retired Canadians surveyed take a more pessimistic view of their likely financial security in retirement. They are as likely as those currently retired to put themselves in the middle comfortable group (48% versus 44% of current retirees), while only one-in-four (24%) expect to have enough money to do everything they want (versus the 38% among those currently retired) and more than one-in-four (28%) expect to be struggling to make ends meet (versus the 18% of current retired who report this).

- Those not yet retired have quite different perspectives as to what will be their primary financial support in retirement. Specifically, considerably fewer of those not yet retired expect to rely on a pension – of either type: 45 per cent said they expect to rely on a government pension (versus 57% of those currently retired), and 34 per cent think they will have a work pension (versus the 53% of the currently retired who cited this as a primary source of their retirement income). Instead, those not yet retired are much more likely to expect to rely on their own savings: fully half (50%) said this will be a key means of support compared to less than one-in-three (30%) of those already retired. Underlining the trepidation many non-retired are feeling, a fair number said they expect to at least partly finance their retirement through downsizing assets (11%) and inheritance or family support (8%).

And, as noted earlier, roughly three-quarters (74%) of not-yet-retired Canadians agree with the statement: “I’m worried about my money lasting my lifetime”. This unfortunate sentiment is widely shared by working Canadians from all walks of life.

| What best describes your situation? | ||

|---|---|---|

| Retired | Non-retired | |

| I (expect to) have enough money to do everything I want | 38% | 24% |

| I (expect to) live comfortably but don’t have money for extras | 44% | 48% |

| Making ends meet is (or will be) a struggle | 18% | 28% |

| What are (do you expect to be) your main sources of retirement income? | ||

|---|---|---|

| Retired | Non-retired | |

| Government pension (Old Age pension) | 57% | 45% |

| Work pension | 53% | 34% |

| Your retirement savings (RRSPs, etc) | 30% | 50% |

| Investments | 13% | 14% |

| Downsizing/selling assets | 6% | 11% |

| Inheritance | 3% | 5% |

| Support from children/family | 1% | 3% |

| Other, specify | 7% | 3% |

PART 3: The Retirement Experience

This research also took a fairly in-depth look at some of the less tangible – but still critical — aspects of retirement with a view to better understanding Canadians’ overall experience with life after work.

Meaning and letdowns

Most retired Canadians do not seem to have trouble extracting meaning from this phase of their life. Three-quarters (76%) of those surveyed disagreed with the sentiment: “I feel like my life does not have as much meaning now that I’m retired.”

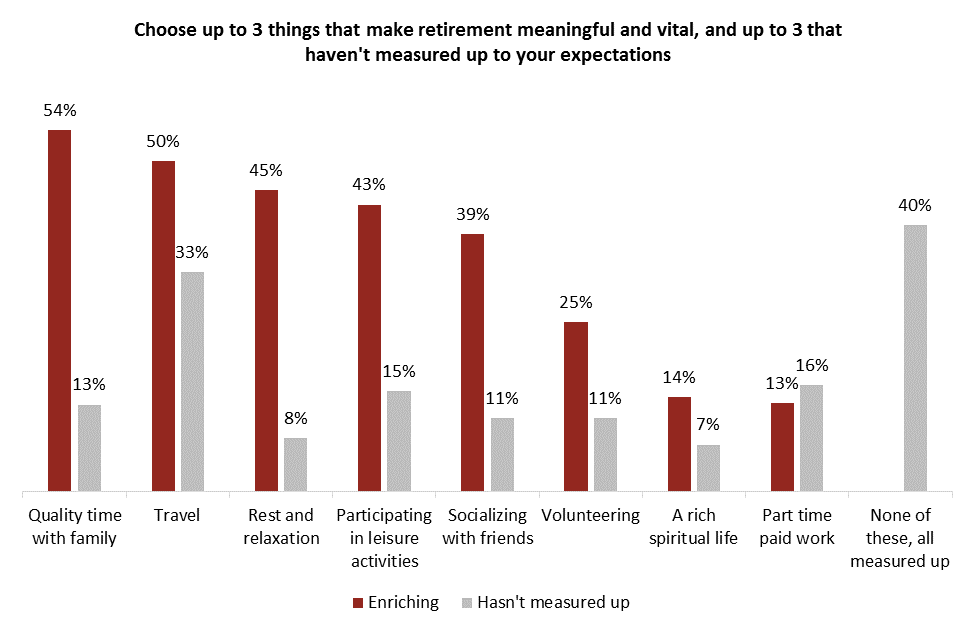

So, what makes retirement meaningful and vital? Those surveyed were asked to choose up to three from a list of eight different possibilities. (Respondents were asked to set aside good health and having enough money and neither was offered on the choice list.)

At the top of the list:

- Quality time with family is a key source of meaning and vitality for most retirees (54%).

- Travel is high on the list as well (50% chose it).

And for many, it’s about having fun:

- Rest and relaxation should not be under-estimated: 45 per cent said this is key for them.

- Almost as many (43%) chose participating in leisure activities as something that adds meaning and vitality to their retirement.

- Socializing with friends was highlighted by four-in-ten (39%).

Rounding out the list:

- Volunteering was selected as a source of meaning in retirement by one-in-four (25%).

- A rich spiritual life is important for one-in-seven (14%).

- Part-time paid work was selected by roughly the same number (13%).

Interestingly, the non-retired group offered similar priorities when asked what they anticipate will enrich their own retirement. They were somewhat more likely than the already retired to highlight travel (61%) and family time (62%), and somewhat less likely to single out socializing with friends (26%) and volunteering (14%).

But what about letdowns? At the end of the survey, retired respondents were asked to consider the same list and highlight anything about retirement that did not happen or did not measure up as hoped. (Again, health and money were set aside for this exercise.)

- Happily, fully four-in-ten (40%) volunteered that none of the areas listed ended up as letdowns, all areas had measured up.

- Travel topped the list of disappointments, selected by one-in-three (33%) respondents.

- Some of the other areas registered as disappointments for fewer retirees:

- Participating in leisure activities (15%)

- Quality time with family (13%)

- Volunteering (11%)

- Socializing with friends (11%)

While just more than one-in-ten (13%) volunteered that “quality time with family” is an aspect of retirement that did not measure up, a separate, focused question indicates this is a source of disappointment for a fair number of retirees. More than one-in-four (28%) agreed with the statement: “I am not able to spend as much time with my family as I would like”.

What’s not to like?

Overall, retired Canadians are enjoying this phase of life – the financial concerns of many notwithstanding. The Angus Reid Institute survey asked retirees to agree or disagree with a number of essential characterizations of “the golden years.” Those not yet retired were asked to contemplate their expectations in these same areas. The comparative results show a lot of cohesion between the two groups, but there are some important and interesting divergences as well.

Again, these survey findings show it’s a lot about the leisure factor. The retired Canadians surveyed voiced very high agreement with some leisure-focused statements, and their non-retired counterparts’ expectations on this front are also very positive:

- “I enjoy (look forward to) having enough time to do the hobbies I have always wanted to do.” A large majority of already retired (86%) and not yet retired (87%) indicated agreement with this statement.

- “I love (look forward to) relaxing and not having to be anywhere.” Both groups were equally enthusiastic about the concept of not having to be anywhere (84% of retired and 85% of non-retired agreed).

Full days

- A similarly large majority of retired Canadians (84%) disagreed with the sentiment: “I am bored and have trouble filling my days” while only 16 per cent agreed. Interestingly, nearly twice as many of the not yet retired (27%) share a concern that they may suffer boredom in retirement.

- Most retired Canadians (59%) feel “connected and involved in the community”. The same number of non-retired (61%) expect to feel this way as well.

- There is a significant demand for better volunteer opportunities. One-in-three (35%) of the retired Canadians surveyed agreed with the sentiment: “I wish I could find a volunteer opportunity that suits me.” Likewise, among those not yet retired, roughly two-in-three (65%) agreed with a similar (though not entirely comparable) statement: “I hope I will be able to find a volunteer opportunity that suits me.”

- Many do feel a bit of a void where work was: 39 per cent of retirees agreed “There are times when I miss going to work.” This is a key area of divergence between the two groups. Fully six-in-ten (62%) of those not yet retired expect they will miss work at times. (Interestingly, the sentiment is considerably more widespread outside Quebec – 67% versus 49% within that province.)

As long as you have your health

Of course, an unpleasant reality about retirement is that ill health can all too easily intrude and interfere mightily – or end altogether – the best laid plans. The survey’s focus was on other, more situational aspects of retirement, but we included one key measure of health status to ensure a fuller picture of the retirement experience (and to facilitate the segmentation analysis described below).

Responses clearly highlight that health concerns cast a shadow on many Canadians’ retirement experience. One-in-three (35%) retired Canadians disagreed with the positive sentiment: “Health issues have not held me back from doing what I want to do”. Roughly the same number of still-working Canadians (33%) share this concern that health issues could well hold them back in retirement.

PART 4: Segmentation analysis: retirement mindsets

In order to fully mine this rich data, Angus Reid Institute researchers conducted a special segmentation (or cluster) analysis. This multivariate analytical technique helps uncover underlying structures and relationships within a given survey data set. Respondents are grouped or “segmented” based on shared attitudinal characteristics. This can powerfully illustrate the different unique “mindsets” surrounding the issue at hand – in this case, retirement.

This segmentation analysis identified four distinct groups of retirees, briefly summarized below:

- “Lovin’ It” – As this segment name implies, members of this group – comprising 29 per cent of the retired population – are happy with this phase of their lives. Very happy indeed. Socio-demographically, these people are somewhat older (67% are over 65) and tend to have more formal education and slightly higher incomes. In addition to having no health concerns (not to be taken for granted at this age level), the “Lovin’ It” group are defined especially by an enviable absence of financial anxiety. Most (66%) acknowledge that they “have enough money to do everything they want” and, indeed, most (65%) enjoy a work pension. They are definitely enjoying retirement, and their overall experience is measuring up as hoped.

- “The Comfortable” describes one-in-four (24%) retired Canadians. This groups tilts towards female representation. The Comfortable share the good health of the “Lovin’ It” group but, alas, not the carefree attitude regarding finances. The vast majority of this group (87%) are worried about outliving their money, even though most (56%) describe their financial situation as “comfortable”. They are much more likely to have experienced disappointments in their retirement (most notably less travel than hoped). Though not bored and enjoying hobbies and relaxing, a fair number (36%) of the Comfortable also miss working.

- “The Strugglers” describes a third segment representing roughly one-in-four (26%) retirees. This group is somewhat younger and many (59%) also retired earlier. Health-wise, this is a mixed bag, roughly evenly split in terms of being held back by health concerns (45% held back, 55% not). Strugglers are indeed struggling with retirement. They are worried about their financial security and (in contrast to the Comfortable) they have reason to be: four-in-ten Strugglers (40%) find it tough to make ends meet and two-thirds (66%) rely on government pension programs. But they have other problems with retirement on several important fronts. Many report disappointments, covering things like travel plans, leisure activities and quality time with family. A large number of Strugglers also admit to being bored in retirement (49%) and struggling with less meaning in their lives (72%). They are least likely to be interested in volunteering and to feel a strong community connection, and most (88%) miss working.

- “The Unhealthy” describes the remaining one-fifth (21%) of Canadian retirees. The Unhealthy, as the segment name implies, suffer from ill health – these retirees are being held back from doing what they want to do by health concerns. Otherwise – though health is obviously an overarching concern, the Unhealthy are quite content with retirement; they are not bored, are enjoying the leisure time, and certainly not missing work. This Unhealthy group also does not have conspicuous money concerns. But they don’t have their health.

Click here for the full report including tables and methodology

Click here for the questionnaire used in this survey

Image – Anukrati Omar/Unsplash

MEDIA CONTACT:

Shachi Kurl, Senior Vice President: 604.908.1693 shachi.kurl@angusreid.org