Four-in-five pessimistic about industry dealing with Trump, but seven-in-10 optimistic overall

December 2, 2025 – Much like the rest of the Canadian economy in 2025, the agriculture and agri-food sector has had significant concerns about the Canada-U.S. relationship. In the second iteration of the Angus Reid Institute and Canadian Agri-Food Policy Institute (CAPI) annual threat assessment, we find these challenges top of mind but hope for many rooted in the opportunities other markets, and the Canadians market itself, present to the industry.

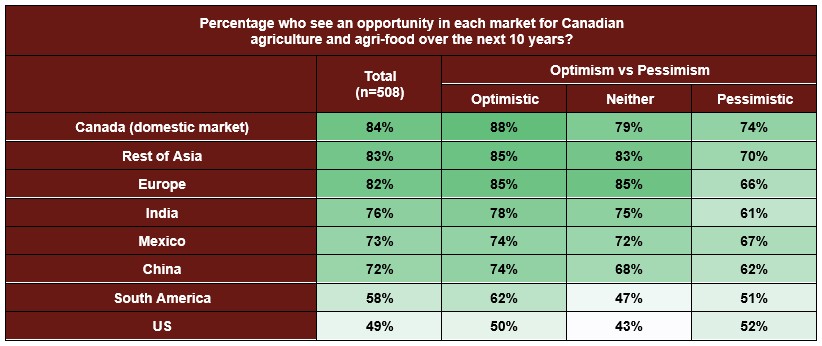

In a survey of more than 500 agriculture and agri-food stakeholders, two-thirds (64%) say the U.S. now represents too large a concentration of industry trade, and that diversification should be a key priority going forward. Fully half (53%) are confident that Canada can make up losses from the U.S. in other markets, though two-in-five show more trepidation (43%). As for where the industry should focus, four-in-five say the domestic Canadian market (84%), Asia (outside of China and India) (83%), and Europe (82%) are significant growth opportunities.

Comparing the industry’s perceived threats from this year to last, trade barriers and protectionism remain top of mind (66% in 2024, 69% in 2025) while extreme weather and climate change both land in the top 10 again. Increasing this year in perceived risk is the political dynamic of the United States, from 32 to 57 per cent. Also rising are concerns over input affordability and commodity price volatility.

The industry clearly perceives challenges but also remains optimistic. Seven-in-10 (70%) say this of the future of agriculture in Canada, though notably, farmers (59%) are less optimistic than those working in government (80%) and civil society (85%).

More Key Findings:

- Views of confidence in government to help either improve or mitigate the top ten challenges shows a trend that is positive compared to 2024, but still largely negative. One-quarter or fewer have confidence across all ten areas

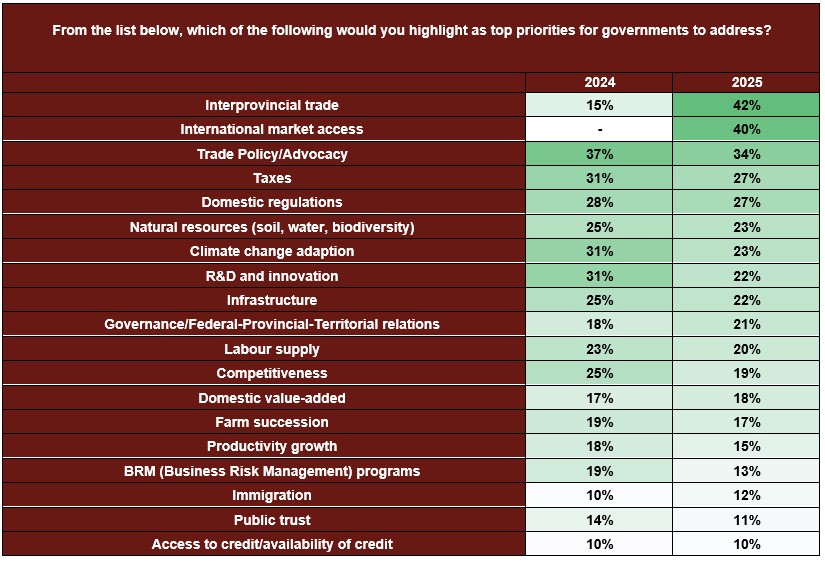

- The top priorities for government according to the industry are improving interprovincial trade (42%), international market access (40%) and trade policy and advocacy (34%). The proportion prioritizing interprovincial trade has risen from 15 per cent last year.

About CAPI

The Canadian Agri-food Policy Institute is an independent, nonpartisan not for profit organization for agri-food leaders to come together, share insights, and advance ideas on emerging issues facing this important sector.

INDEX

Introduction

Part One: The Elephant in the Room: The U.S. relationship

-

Canadians look abroad, but see opportunity at home, too

Part Two: Threats to the sector

-

Top 10 Threats in 2025 overall

-

Largest increases

-

Largest decreases

-

How manageable are these top challenges?

-

Policy and regulatory follow-up

Part Three: Priorities, optimism, and confidence

-

Top priorities for government have shifted

-

Despite challenges, optimism remains high in the industry

-

The optimistic see opportunity

-

Confidence in government and private sector has risen but is still very low

Introduction:

This is the second study in partnership between Angus Reid Institute and Canadian Agri-Food Policy Institute. The goal of this research is to understand and inform the priorities, risks, and perspectives involved in the Canadian agriculture and agri-food sector. In order to understand the challenges and opportunities going forward, ARI and CAPI conducted a survey of 508 individuals working in the agriculture sector. This includes 198 farmers 60 members of government, as well as others across the industry. Note that in some cases smaller sample sizes are valuable but should be interpreted with caution.

Part One: The Elephant in the Room: The U.S. relationship

The Canadian economy has faced historic levels of uncertainty during 2025, with threats and implementation of tariffs on Canadian goods. Consumers and producers alike have been on pins and needles seemingly every month, waiting to see what Donald Trump’s whims will trigger. Canada’s supply management system has been in the American crosshairs for years and continues to garner scrutiny. Meanwhile, with rising costs for inputs and equipment, agriculture workers on both sides of the border voice anxiety and frustration.

Asked about their views for the four-year term of Trump, four-in-five (78%) agriculture and agri-food stakeholders are pessimistic, with one-in-five (22%) voicing optimism:

Three-in-10 within the industry say these tariffs aren’t really a concern for them as they feel insulated from any potential tariff action. A similar group (27%) say they are exposed but would be able to weather it for the full term if it lasts that long. Others, however, are less confident, including farmers and those across the industry, whose livelihoods are threatened:

Perhaps unsurprisingly, the mood of the sector is that U.S. market concentration is too high. Two-thirds (64%) say this, while one-quarter (25%) are comfortable, and few would work to increase trade in this market.

Farmers are most comfortable with the current market dynamics between the two countries, though 56 agree that the concentration in the U.S. is too high.

Supposing that Canada did try to concentrate less in the United States, moving elsewhere to make up the difference, stakeholders are divided about how successful this would be. Half (53%) are confident that these losses could be made up, while 43 per cent are not confident:

Canadians look abroad, but see opportunity at home, too

The domestic market does hold considerable appeal within the industry, as the focus on interprovincial trade barriers has elucidated in recent months. Two-in-five (41%) say they would prefer to focus on building the market at home rather than international relationships, though trade abroad is still seen as preferable by the majority:

Expanding trade at home is seen as among the most significant opportunities over the next decade. Similar numbers within the industry say this, along with the rest of Asia (outside of China and India), and Europe, represent the highest level of opportunity. India, Mexico, and China are also chosen by more than seven-in-10, while the United States, once the nation’s largest ally, is seen as an opportunity by half.

Supposing there is a disruption in agriculture and agrifood between the two countries, just one-in-three (33%) are confident that Canada can mitigate these impacts. Others have little or no confidence, feeling much more at the mercy of the U.S. administration:

Part Two: Threats to the sector

In order to establish tiers of risk, given the robust nature of the agriculture and agri-food industry in Canada, respondents were given lists separated into five distinct categories:

- Environmental

- Financial/Economic

- Domestic

- Production

- International

Top 10 Threats in 2025 overall

From a list of 35 different potential risks, eight were chosen by more than half of stakeholders, with trade barriers and protectionism, as well as extreme weather taking the top two positions. One recent study found that more than three-quarters of farmers and ranchers in Canada had experienced “drought, heat waves, floods, wildfires, hail, tornadoes, or new pests and diseases in the past five years.” Meantime, trade barriers and protectionism have been a nationwide, in fact worldwide, discussion in 2025 with the Trump administration implementing tariffs. This only adds to the tariff tit-for-tat between Canada and China, which has seen the latter put a tariff on Canadian canola meal and oil in response to Canada’s electric vehicle tariff.

The policy and regulatory environment is still a top concern, but has been reduced, perhaps given the expectation of a new government. Note this survey was fielded during the federal election campaign but before the result was known:

Largest increases

Largest increases

This year has seen the elevation of two key issues into the risk-profile perceived by stakeholders over the next 10 years – recession and the political dynamic in the United States. These two are clearly intertwined given the risk of recession has risen considerably since Donald Trump took office in January. Last year 16 per cent were concerned about recession while this year 42 per cent say the same. There has also been a 25-point increase on risk posed from dynamics south of the border:

Largest decreases

Largest decreases

Some threats are going in the opposite direction, foremost, the concern over interest rates, which have been cut by the Bank of Canada seven times since last May. The threat of poor public trust in agri-food has also dropped by nine points, from 29 to 20:

How manageable are these top challenges?

How manageable are these top challenges?

Nearly all of these top threats are seen as “already a problem” (see detailed tables) as opposed to threatening the sector further down the line, but there is some variance in how many are viewed as manageable. Climate change and the U.S. political dynamic are both most likely to be viewed as extremely difficult to overcome, while infrastructure is seen as the most manageable.

Policy and regulatory follow-up

Among those stakeholders who said that the policy and regulatory environment was a concern (60%), a follow-up question was posed about the factors driving this concern. Half say that there is an unnecessary regulatory burden to overcome, while two-in-five said that a misalignment of government and sector priorities make this a challenge. Close to two-in-five (37%) also said that agriculture and agri-food are just not understood by those working outside of production:

Part Three: Top priorities for government have shifted

While threats are one aspect of the conversation, priorities are another. In 2024, trade policy and advocacy was the top priority from agriculture stakeholders when they considered where the government should focus its efforts. This, followed closely by taxation, research and development, and climate change adaptation. This year, ARI and CAPI decided to add two other priorities, given the significant disruption caused by President Trump. Both of those items – interprovincial trade and international market access -are chosen by two-in-five stakeholders, putting them atop the list.

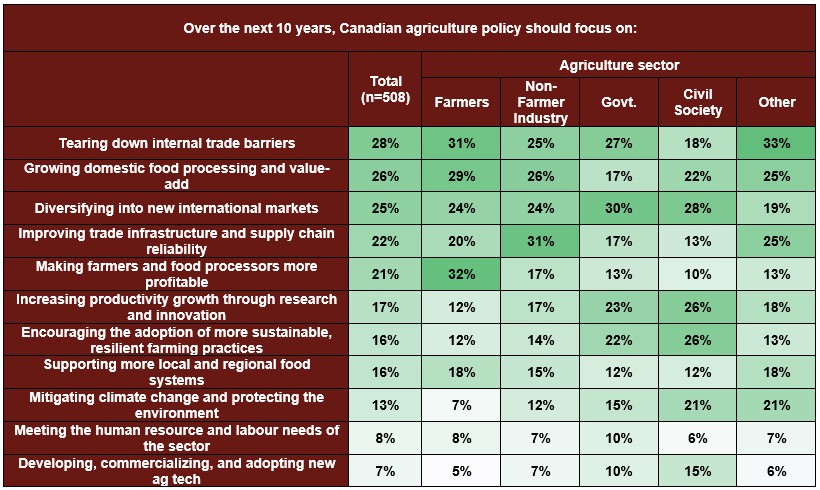

Thinking about the next 10 years, the issue of internal trade barriers and interprovincial trade again shows its importance. Tearing down internal trade barriers is the to issues for farmers (31%) aside from simply making farmers and food processors more profitable (32%). Growing domestic food processing and valued-add is also key in the minds of many. Exports of food and beverage processing have been growing steadily in recent years, though face significant uncertainty in this current tariff-intensive environment:

Thinking about the next 10 years, the issue of internal trade barriers and interprovincial trade again shows its importance. Tearing down internal trade barriers is the to issues for farmers (31%) aside from simply making farmers and food processors more profitable (32%). Growing domestic food processing and valued-add is also key in the minds of many. Exports of food and beverage processing have been growing steadily in recent years, though face significant uncertainty in this current tariff-intensive environment:

Despite challenges, optimism remains high in the industry

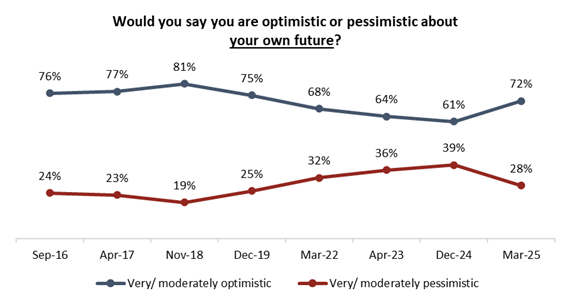

One of the most notable findings in this year’s data is the same as last year’s, that is, that the industry remains optimistic, even while being pessimistic about Trump. Asked about their views of the future of the sector, 70 per cent are optimistic, an increase from last year. One-in-seven (15%) are very positive, while others are more muted but still feeling optimistic:

These views put the agriculture and agri-food sector in line with the rest of the population, both last year and this year, in terms of their overall optimism.

These views put the agriculture and agri-food sector in line with the rest of the population, both last year and this year, in terms of their overall optimism.

Positive sentiments are lower among farmers than other working in the sector, as was the case in 2024. That said, optimism among all groups has either improved or remained steady:

The optimistic see opportunity

The optimistic see opportunity

Some of this optimism may be credited to the opportunity that Canadian agriculture and agri-food workers perceive available to them. Opportunities in other markets are viewed as widespread among most and even more so among those who have a positive view about the future:

Confidence in government and private sector has risen but is still very low

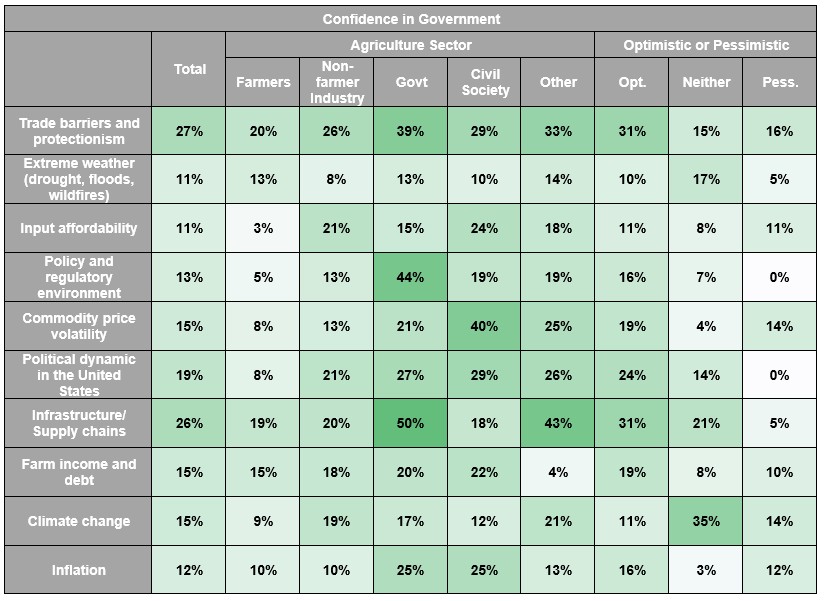

Views of confidence in government show a trend that is positive, but still overall negative. The proportion of those in the industry feeling that the current policy framework will help the industry to overcome these challenges has increased for most threat areas but remains well below the majority mark. The sector shows the most hope for government assistance in overcoming trade barriers and infrastructure challenges, but in both cases does not surpass one-in-four:

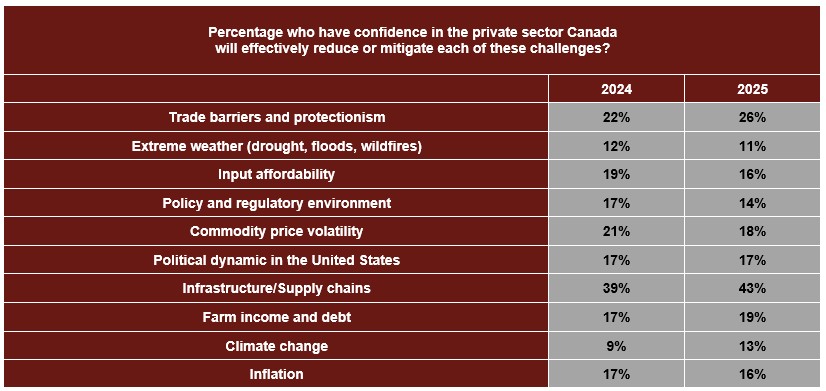

The private sector is in most cases viewed as more suited to help reduce or mitigate challenges, but again, assessments are hardly rosy:

The private sector is in most cases viewed as more suited to help reduce or mitigate challenges, but again, assessments are hardly rosy:

Even among the optimistic, confidence in government does not increase beyond three-in-10. Interestingly, those who work in government are much more optimistic about their ability to help:

Even among the optimistic, confidence in government does not increase beyond three-in-10. Interestingly, those who work in government are much more optimistic about their ability to help:

METHODOLOGY

The Angus Reid Institute in partnership with the Canadian Agri-Food Policy Institute conducted an online survey from February 19 – April 1, 2025 among a sample of 508 Canadian adults who are members of Angus Reid Forum (259) or surveyed online by CAPI (249). For comparison purposes only, a probability sample of this size would carry a margin of error of +/- 4 percentage points, 19 times out of 20. Discrepancies in or between totals are due to rounding. The survey was self-commissioned and paid for by ARI. Detailed tables are found at the end of this release.

For detailed results by age, gender, region, education, and other demographics, click here.

For PDF of full release, click here.

For questionnaire, click here.

MEDIA CONTACT:

Elise Bigley, Director, Strategic Projects for CAPI bigleye@capi-icpa.ca

Dave Korzinski, Research Director: 250.899.0821 dave.korzinski@angusreid.org