Two-thirds who say their housing costs make their budget tight also say it’s difficult to feed their families

March 7, 2022 – As the Bank of Canada wields rate hikes to battle inflation, it does so with the cost of housing in mind.

New data from the non-profit Angus Reid Institute finds budgets already squeezed by mortgages – and rent – before the slow climb of the benchmark interest rate begins. Three-in-five (58%) Canadian mortgage holders say their payments crowd out other portions of their budget. Three-quarters (74%) of renters say the same of their rent.

Among this group of homeowners and renters, two-thirds (65%) say it’s meeting the household food budget that is becoming difficult. Almost all (92%) have done something – from cutting out takeout (72%) or switching to cheaper brands at the grocery store (62%) – to adjust to food inflation.

Inflation, the runaway horse the Bank of Canada is trying to wrangle this year, is clearly not doing Canadians any favours. But few homeowners with a mortgage or renters have wiggle room to accommodate increases to the largest line item in their budget as interest rates rise. Seven-in-ten who say their rent or mortgage payments cause them to spend less elsewhere also say there’s no room in their monthly budget for an unexpected expense of more than $1,000.

More Key Findings:

- Four-in-five (83%) renters with a child under the age of 13 in their household say their rent eats into their budget each month; seven-in-ten (71%) of those in households without young children say the same.

- Half (51%) of those who say their rent or mortgage is no problem say they stress about money. For the rest of mortgage and renters, nine-in-ten (87%) say the same.

About ARI

The Angus Reid Institute (ARI) was founded in October 2014 by pollster and sociologist, Dr. Angus Reid. ARI is a national, not-for-profit, non-partisan public opinion research foundation established to advance education by commissioning, conducting and disseminating to the public accessible and impartial statistical data, research and policy analysis on economics, political science, philanthropy, public administration, domestic and international affairs and other socio-economic issues of importance to Canada and its world.

INDEX

Part One: The Canadian housing picture – who are the owners and renters?

Part Two: The costs of housing

-

Budget already tight for majority of Canadians with mortgage

-

Most renters curbing discretionary spending

-

Those with children in household are more likely to feel pinched by their rent, mortgage

Part Three: The impact of the high cost of housing on household budgets

Part One: The Canadian housing picture – who are the owners and renters?

Canadians, historically, have been a nation of homeowners. The majority of Canadians own their own home dating back to the 1970s, while historically around one-third of Canadians rent.

Three-in-five in ARI’s sample say they own their home, while three-in-10 rent. One-in-10 say they have other arrangements, including living with their parents or another family member rent-free.

This aligns with the most recently available census data. In 2016, Statistics Canada reported 63 per cent of Canadians owned their home.

Homeownership rates change naturally with age. Older Canadians are more likely to own their own home and younger Canadians are more likely to be renters, though there is a gender discrepancy to this last point. More than two-in-five (45%) women aged 18- to 34-years-old say they are renters, more than those who say they are owners. Men that age are slightly more likely to be owners than renters:

There is also a natural age discrepancy when it comes to whether Canadians who own a home are paying a mortgage. Younger Canadians are less likely to own their residence outright, but there is a notable gap at the age of 54-years-old. For Canadians older than 54, a majority say they are not paying a mortgage, while one-in-five (22%) Canadians aged 45- to 54-years-old say the same:

For a previous study, ARI created a Cost of Living Index to illustrate how Canadians’ household budgets are coping with the rapidly increasing cost of living in the country. The Index separated respondents into four groups – Staying Ahead, Keeping Up, Losing Pace, and Left Behind – based on their self assessments on how they were faring with the cost of housing, grocery bills, and child care and the amount of wiggle room in their budget each month.

Related: The Cost of Living Index

Half of those who are Left Behind by the rising cost of living are renters. For all other groups, the majority are homeowners, including approaching three-quarters (73%) of those who are Staying Ahead of rising cost of living:

For the two-in-five in the Left Behind group who own their own home, most (85%) have a mortgage on it. At the other end of the Cost of Living Index, half (48%) of the Staying Ahead say they don’t have a mortgage on their home:

Part Two: The costs of housing

Inflation is the spectre that haunts almost every economic conversation in Canadian kitchens and living rooms these days. Canadians are increasingly feeling the pinch in their wallet and are changing their consumer habits at the grocery store and elsewhere.

Related:

- Falling Behind: 53% of Canadians say they can’t keep up with the cost of living

- Price Check: Four-in-five say they’ve changed food buying habits because of increasing costs

Canada’s central bank is carefully wielding a weapon to fight inflation – the benchmark interest rate, which affects the cost of money across the country – with an eye on a hot housing market that gained a significant number of mortgaged buyers during the pandemic. Last week, for the first time since 2018, the Bank of Canada raised the benchmark rate. It now sits at 0.5 per cent, up from a rate of 0.25 per cent set throughout the pandemic to help keep the economy running as COVID-19 forced business closures and layoffs.

The bank is expected to continue to raise rates this year to fight inflation, and the impact could be significant on those with variable rate mortgages and those whose fixed rate mortgages come up for renewal soon.

Budget already tight for majority of Canadians with mortgage

For most mortgage holders, the cost of payments is already squeezing their budget. While two-in-five (42%) say they can easily manage their payments, more (46%) say they must watch their discretionary spending. One-in-10 (11%) say it curbs their lifestyle and a handful (1%) say making their high mortgage payments is a real struggle:

Homeowners with annual household incomes of less than $100,000 are less likely to say they have money left over after their mortgage payments than those in higher income households. Half (49%) of households earning six figures annually say they can manage their mortgage payments easily, while one-third of those in households earning less say the same. Instead, fully half (53%) of lower-income households say their mortgage payments require them to watch their discretionary spending:

Men and women have slightly diverging views about just how much stress their mortgage is causing. Consider that one-in-three women (34%) say their mortgage is easily handled, while half of men (49%) say the same:

Most renters curbing discretionary spending

Renters are having a more difficult time with the high cost of housing than mortgage holders on balance. This, as vacancy rates in many cities plummet and squeeze out low-income individuals. One-quarter of Canadians renters say they can comfortably afford this expense, with money left over. Approaching half (45%) say they have to watch their spending on extras, 17 per cent say the amount they pay for rent curbs their lifestyle and one-in-ten (12%) are struggling to make ends meet because of how much they pay in rent:

One-third of renters over the age of 54 say covering their rent each month is no sweat, the most of any age group. For 35- to 54-year-olds, one-in-five (19%) say instead it’s a struggle to make ends meet because of how much they pay in rent. Unlike mortgage holders, male and female renters hold near-identical views on their financial experiences:

Those with children in their household are more likely to feel pinched by their rent, mortgage

Homeowners with younger children in their household are close to equally likely to say they find their mortgage payments easy or difficult compared to those who do not have children (see detailed tables). This is less the case for renters. For those who do not own their residence, three-in-ten (29%) in households without children under 13 say they have an easy time paying their rent; one-in-five (18%) living with a kid under 13 say the same. The majority in both groups face challenges in covering this essential cost of living:

Part Three: The impact of the high cost of housing on household budgets

Respondents were asked to assess how well their monthly budget could accommodate a surprise expense. Overall, renters are less likely to have room to spare for unexpected bills than homeowners with mortgages. One-quarter (23%) of renters say they could not manage any unexpected expense, nearly double the number of mortgage-holders who say the same (12%). One-third of renters say they could handle an unplanned-for bill of $1,000, while just over half (54%) of homeowners with a mortgage feel the same:

For those who find their rent or mortgage payments easy to handle, three-quarters say they could handle an unexpected expense of over $1,000. For others who say the cost of their rent or mortgage eats into their budget for other things, at least three-in-five say they wouldn’t be able to accommodate an unplanned bill of more than $1,000:

*Smaller sample size, interpret with caution

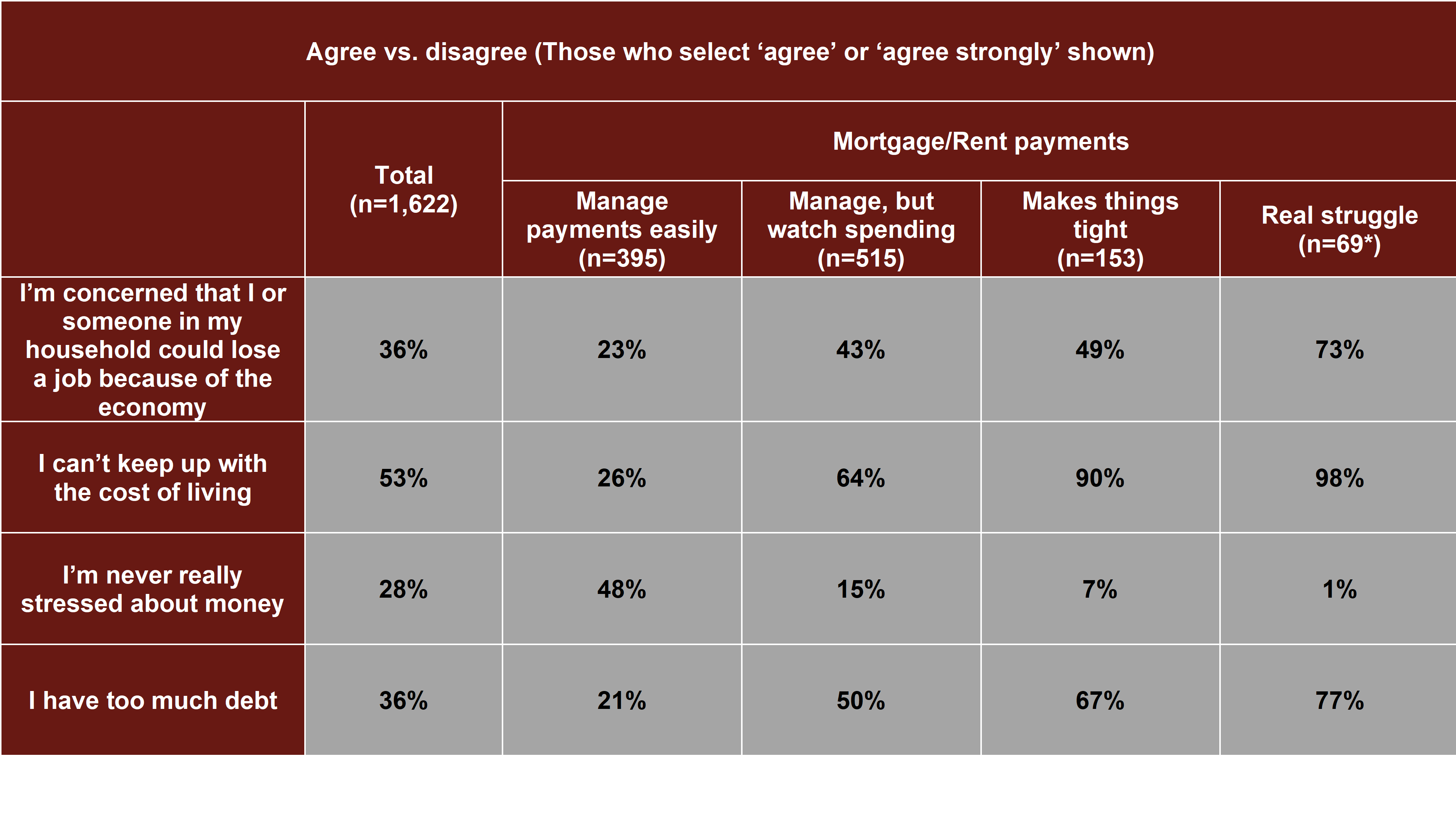

Other money worries are also more plentiful among those whose mortgage or rent occupies a significant portion of their budget. Nearly all who say the high cost of their housing makes their budget tight or a real struggle say they feel left behind by the rising cost of living. Few in those groups say they are never stressed about money and at least two-thirds say they are carrying too much debt:

*Smaller sample size, interpret with caution

Four-in-five who feel they have plenty left over after they’ve paid their rent or mortgage also say it’s easy to feed their household. For every other group, a majority say the opposite:

*Smaller sample size, interpret with caution

Rising food prices have apparently had a larger impact on the behaviours of Canadians who are having a harder time with their monthly rent or mortgage payments. For those who say they can easily cover their rent or mortgage each month, three-in-ten (28%) say they haven’t changed their food-buying habits, a proportion much higher among those who find their monthly housing costs more difficult.

Instead, a majority of those who say the cost of their rent or mortgage eats away at their budget also say they’ve cut down on dining at restaurants and are saving money at the grocery store by switching to cheaper brands:

*Smaller sample size, interpret with caution

As for other spending cuts, more than two-in-five (44%) who say they are easily handling their rent or mortgage say they haven’t done any. For the rest of renters and mortgage holders, nearly all have adapted their spending in some way, including majorities who have cut back to the essentials and delayed a major purchase:

*Smaller sample size, interpret with caution

Survey Methodology:

The Angus Reid Institute conducted an online survey from Feb. 11-13, 2022 among a representative randomized sample of 1,622 Canadian adults who are members of Angus Reid Forum. For comparison purposes only, a probability sample of this size would carry a margin of error of +/- 2.5 percentage points, 19 times out of 20. Discrepancies in or between totals are due to rounding. The survey was self-commissioned and paid for by ARI.

For detailed results by age, gender, region, education, and other demographics, click here.

For detailed results by the Cost of Living Index and whether or not there is a child under the age of 13 in the household, click here.

For detailed results by housing situation and how respondents feel they handle their mortgage or rent payments, click here.

To read the full report, including detailed tables and methodology, click here.

To read the questionnaire in English and French, click here.

Image – Tierra Mallorca, Unsplash

MEDIA CONTACT:

Shachi Kurl, President: 604.908.1693 shachi.kurl@angusreid.org @shachikurl

Dave Korzinski, Research Director: 250.899.0821 dave.korzinski@angusreid.org