One-quarter want further rate hikes; financial pessimism reaches 13-year high

May 24, 2022 – As inflation reaches a 31-year high, Canadians are more likely to want the Bank of Canada to stand-pat than continue to push up the cost of borrowing.

A new study from the non-profit Angus Reid Institute finds approaching half (45%) of Canadians say they would like the country’s central bank to hold firm at one per cent for its key benchmark rate and see how that affects inflation before taking further action. One-quarter (27%) would continue to increase the rate in a more aggressive attempt to mitigate rising prices, while half that number (13%) say that they would keep rates low as they worry about the impact any changes may have on the housing and investment markets.

While inflation is one economic bogeyman hounding the country, Canadians are facing other financial challenges. One-in-five (22%) say they have major debt concerns currently, while another two-in-five (42%) say this is a more minor problem, but still a source of stress. For the one-in-five who have heightened debt concerns, most say they are cutting back on “going out”, trimming phone and streaming expenses wherever possible, changing their diet to consume cheaper foods, and driving less.

As the BoC debates further rate hikes this summer to ease inflation, Canadians expectations are more negative now than they have been over the last decade. Nearly three-in-ten (28%) say that they expect to be worse off financially by this time next year – a seven-point increase in the number who said this last year, and the highest mark recorded in 13 years of tracking.

More Key Findings:

- The percentage of Canadians who say they are worse off now than they were 12 months ago is also at its highest mark since 2010 at 36 per cent (34% in 2021, 32% in 2020).

- The Angus Reid Institute’s Economic Stress Index finds 22 per cent of Canadians Struggling, 25 per cent Uncomfortable, 26 per cent Comfortable and 27 per cent Thriving.

- One-third (32%) of Canadians express difficulty in paying for their housing costs, whether renting or paying a mortgage. This includes 93 per cent of those who are categorized at Struggling.

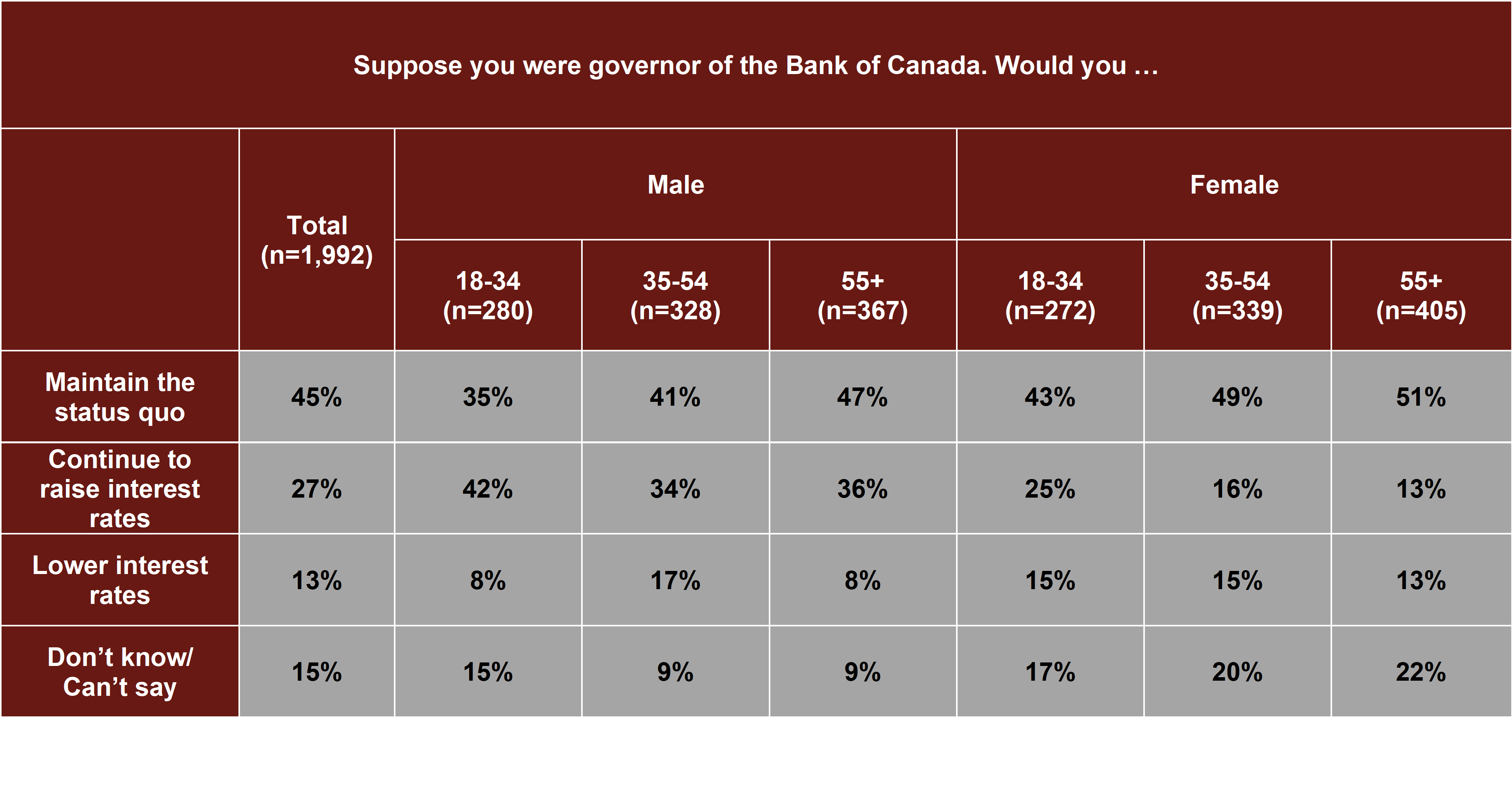

- Men of all ages are considerably more likely than women to say that the Bank of Canada should increase interest rates further (37% to 17% overall).

About ARI

The Angus Reid Institute (ARI) was founded in October 2014 by pollster and sociologist, Dr. Angus Reid. ARI is a national, not-for-profit, non-partisan public opinion research foundation established to advance education by commissioning, conducting and disseminating to the public accessible and impartial statistical data, research and policy analysis on economics, political science, philanthropy, public administration, domestic and international affairs and other socio-economic issues of importance to Canada and its world.

INDEX

Part One: Taking the temperature of Canadians’ household finances

-

The Economic Stress Index

-

One-third report deteriorating finances over the last year

-

Half of Canadians say it’s difficult to afford to feed their household

Part Two: The debt picture

-

Household debt is a source of stress for two-thirds

-

Canadians stressing over debt have cut back on going out, streaming services, driving

Part Three: What should the Bank of Canada do?

-

More than two-in-five want BoC to maintain rates where they are; one-quarter want higher rates

-

Past CPC voters more likely to want BoC to lower rates again

Part One: Taking the temperature of Canadians’ household finances

As Canadians leave pandemic health restrictions behind, they are left to deal with the economic ramifications of pandemic public policy. Two years of low interest rates and generous government spending has resulted in significant inflation – 6.8% in April, a 31-year high. Prices for everything are climbing, including key staples like groceries and gasoline. Both of those are further affected by Russia’s invasion of Ukraine, bringing war to a key global region for both food and energy.

The Economic Stress Index

In an attempt to measure the economic pressure on Canadians during this tumultuous economic time, ARI created the Economic Stress Index in January. The index analyzes a number of core variables involving relative levels of concern over debt, housing costs, and household food costs, as well as respondents’ self-appraisal of the effect of the past 12 months on their finances as well as the year to come.

The ESI yields four groups: the Thriving (27% of Canadians), the Comfortable (26%), the Uncomfortable (25%) and the Struggling (22%):

The current economic stress is not felt equally across the country. Those living in Manitoba (29%), Saskatchewan (27%), and Atlantic Canada (26%) are more likely to be Struggling. As well, majorities in Saskatchewan, Alberta and Atlantic Canada fall in the bottom half of the ESI. One-third (35%) of Quebecers are Thriving, the most of any region in the country:

Perhaps this is reflective of the asymmetrical effect inflation has had on the country. In the Atlantic provinces, where one-quarter (26%) are struggling, the price of food has climbed faster than the national average, according to Statistics Canada. As well, the cost of energy, including electricity, gasoline and other types of fuel, has climbed on the east coast in the last year faster than other regions in the country.

Meanwhile, though Saskatchewan has come out better than some provinces when it comes to Statistics Canada’s inflation measures, it was the only Canadian province to see its GDP drop in 2021 – the effect of a severe drought that devastated the province’s agriculture industry. Notably, Manitoba, where three-in-ten are Struggling, experienced only a 1.2 per cent growth in GDP last year, the second lowest rate in the country.

Canadians in the middle of their career – aged 35 to 54 – are more likely to be Struggling than other demographics. As well, they are the only demographic which has a majority in the lower half of the index (see detailed tables).

One-third report deteriorating finances over the last year

As inflation continues to batter Canadian wallets, one-third (36%) say they are in a worse financial situation than they were in a year ago. One-quarter (24%) say the opposite, that their financial picture has improved in the last 12 months.

Since the pandemic began in 2020, Canadians are much more likely to say one or the other – that their finances have improved or deteriorated in the last year. Prior to the pandemic, at least half would say that their finances have remained relatively stable. Perhaps this is a reflection of COVID-19’s impact on inequality. Experts worry that the pandemic has widened the gap between the rich and the poor.

More than four-in-five (84%) of the Struggling say their financial picture has worsened over the last year. The Uncomfortable are as likely to say the same (43%) as to report treading water in the last 12 months. Meanwhile, half of the Thriving say they are in better shape financially than they were one year ago:

In the first two years of the pandemic, financial optimism outweighed pessimism at this time of year. Now three-in-ten (28%) believe they will be in a worse position financially next year, more than the one-quarter (24%) who believe the opposite. That former figure represents a peak since 2010 in financial gloom for Canadians:

There is little optimism among the Struggling that their situation will improve over time. Three-in-five (63%) in that group believe they will be worse off financially one year from now. A plurality (36%) of the Uncomfortable agree. For the Thriving, nearly all believe they will be in the same position financially (48%) or doing even better (43%):

Half of Canadians say it’s difficult to afford to feed their household

Statistics Canada reported that food prices rose 8.7 per cent year over year in March, a rate unseen since 2008. The expectation is that a family of four will pay nearly $1,000 more for food in 2022 than they did in 2021.

As many Canadians say it is difficult to feed their household (49%) as say that it is instead easy (48%). Three years ago, three-in-five (62%) said they could easily afford to feed their household:

Food inflation is not impacting Canadian’s budgets evenly. Nearly all (99%) of the Struggling say it is difficult to afford to feed their household. On the other end of the Economic Stress Index, nearly all (98%) of the Thriving have no trouble putting food on the table (see detailed tables).

Rent and mortgage payments are another factor pressuring Canadian’s finances. As the Bank of Canada increases interest rates to wrangle inflation, mortgage rates will rise and those increases will have a reciprocal effect on rent.

Nationally, three-in-five (63%) say the cost of their mortgage or rent is easy or manageable. A significant minority – one third (32%) – say instead it is tough or difficult to pay that bill each month. That latter group includes nearly all (93%) of the Struggling. For all other groups along the Index, a majority say they find their monthly housing payments easy or manageable.

Part Two: The debt picture

Over the course of the pandemic, consumer debt climbed to record levels. In the fourth quarter of 2021, Statistics Canada reported that the ratio of household debt to disposable income reached 186.2 per cent, above the previous record high of 184.7 per cent in the third quarter of 2018. This debt complicates the picture for the Bank of Canada as it raises interest rates to fight inflation.

Household debt is a source of stress for two-thirds

One-in-five (22%) Canadians report that their household debt is a major source of stress. For a further two-in-five (42%), it is still a source of stress, but more of a minor one. One-third have no problem with the amount of debt their household holds (19%) or hold no debt at all (17%).

Along the Economic Stress Index, only the Thriving are mostly unburdened with their levels of debt. For that group, one-third hold no debt (33%) and half don’t consider it a source of stress (52%). For all other groups, a majority carry some amount of stress for their level of debt, including two-thirds of the Struggling who say they experience major stress over their household’s debt:

Canadians stressing over debt have cut back on going out, streaming services, driving

Canadians feeling major anxiety over their levels of debt have adjusted their spending habits. Most (86%) have stopped dining out as much. Majorities, too, have cut back on streaming services and phone bills (69%), switched to cheaper brands at the grocery store (66%), are driving less (63%) and are cancelling family activities like hockey or dance lessons (57%):

These changes in consumer behaviours are much more common among the Struggling than other groups along the ESI. For the Thriving, 99 per cent do not see their debt as a major source of stress. That’s only the case for one-third of the Struggling:

Part Three: What should the Bank of Canada do?

In April, the Bank of Canada increased its key interest rate from 0.5 per cent to one per cent as a counteraction against the record levels of inflation the country is seeing. It was the largest interest rate hike the central bank had made in 20 years. The Royal Bank of Canada expects the BoC to bump rates by 0.5 per cent again in June and July and sees the overnight rate reaching 2.5 per cent by the end of the year. The overnight rate has not been that high since October 2008.

The impact of rising interest rates will be felt by Canadians on their mortgages, whether they are on a variable rate or looking to renew their fixed rate mortgages. As well, it’s expected rising interest rates will cool the housing market by decreasing demand as buyers will not be able to qualify for as large as a mortgage as before, or are pushed out of the market entirely.

More than two-in-five want BoC to maintain rates where they are; one-quarter want higher rates

The largest group of Canadians (45%) want to wait to see how the Bank of Canada’s April interest rate hike affects the market before the Bank acts again. One-quarter (27%) would push interest rates even higher, double the number who instead want the BoC to reverse course and lower interest rates (13%).

Men aged 18- to 34-years-old and older than 54 are the least likely to want the BoC to lower rates. Meanwhile, men are more likely than women to want interest rates to continue to rise:

Past CPC voters more likely to want BoC to lower rates again

While pluralities of all partisans prefer the BoC to hold course and wait to see the effects of its latest rate hike before taking further action, past CPC voters are twice as likely as other past party supporters to want Canada’s central bank to move in the other direction and lower interest rates.

These data come as a row over management of the Bank of Canada has erupted amongst the Conservative caucus. Conservative MP and leadership candidate Pierre Poilievre said during the CPC leadership debate that, if he became prime minister, he would fire BoC governor Tiff Macklem. Conservative MP Ed Fast, the party’s finance critic, called out Poilievre in response, saying the party “loses credibility” when it doesn’t respect the independence of institutions like the BoC. Conservative MPs who support Poilievre were reportedly angered by Fast’s comments, and, hours later, Fast, who is also the co-chair of the CPC leadership campaign of Poilievre rival Jean Charest, resigned from his duties as finance critic.

Those living in the lowest income households are half as likely (16%) to believe the Bank of Canada should continue to raise interest rates than those in households earning $100,000 or more annually. As well, Canadians living in households earning less than $25,000 annually are the most likely of all income brackets to say the BoC should instead lower interest rates.

Meanwhile, approaching half of households earning six figures per year believe the bank should wait to see how the most recent rate hike affects inflation before taking further action. And one-third in those households would like to see further interest rate hikes right away:

Survey Methodology

The Angus Reid Institute conducted an online survey from May 4 – 6, 2022 among a representative randomized sample of 1,992 Canadian adults who are members of Angus Reid Forum. For comparison purposes only, a probability sample of this size would carry a margin of error of +/- 2.5 percentage points, 19 times out of 20. Discrepancies in or between totals are due to rounding. The survey was self-commissioned and paid for by ARI.

For detailed results by age, gender, region, education, and other demographics, click here.

For detailed results by the Economic Stress Index, click here.

To read the full report, including detailed tables and methodology, click here.

To read the questionnaire in English and French, click here.

Image – Bank of Canada/Flickr

MEDIA CONTACT:

Shachi Kurl, President: 604.908.1693 shachi.kurl@angusreid.org @shachikurl

Dave Korzinski, Research Director: 250.899.0821 dave.korzinski@angusreid.org

Jon Roe, Research Associate: jon.roe@angusreid.org